Commercial Real Estate Underwriting Explained

Every commercial real estate deal starts with one question. Does this deal make financial sense? That question is answered through underwriting. Underwriting is the process of checking a property’s numbers before money changes hands. It is how lenders decide whether to give a loan. It is also how investors decide whether to buy a property.

Without underwriting, you are guessing. You might overpay for a property and might borrow too much, and buy something that looks good on the surface but loses money every month. Underwriting protects you from all of that. It turns a feeling into a fact-based decision.

The good news is that underwriting is not as hard as it sounds. You do not need a finance degree to understand it. You just need to know the right questions to ask and the right numbers to calculate. This guide breaks everything down in plain language. You will learn what underwriting is, why it matters, how lenders and investors use it, and what the key numbers mean — with real examples that make it easy to follow.

According to Deloitte’s 2026 Commercial Real Estate Outlook, new CRE loan volume grew by 13% from late 2024 and by over 90% from the same period the year before. More deals are being done. More loans are being approved. Understanding underwriting right now puts you in a stronger position in a market that is picking up fast.

By the end of this guide, you will know how to read a deal the way a lender does. That knowledge is worth a lot — whether you are trying to get a loan, buy a property, or simply understand what is happening in your portfolio.

What Is Commercial Real Estate Underwriting and Who Does It

What Commercial Real Estate Underwriting Really Means

Commercial real estate underwriting is the process of studying a property’s financial health before a loan is approved or a deal is closed. It looks at how much money the property makes, how much it costs to run, how much debt it can carry, and how risky it is to own. Think of it like a health check for a building. A doctor checks your blood pressure, heart rate, and test results before telling you if you are healthy. An underwriter checks a property’s income, expenses, and debt before telling you if the deal is safe. Both processes use data to find the truth.

Here is a simple real-world example. You want to buy a 20-unit apartment building. The seller says it earns $600,000 per year and is 95% full. Underwriting is how you check if that is true. You look at the actual leases. You check the real expense records and calculate what the building truly earns after all costs. Then you decide if the price makes sense.

Who Participates in Commercial Real Estate Underwriting

| Participant | Role in the Deal | What They Analyze | Why It Matters |

|---|---|---|---|

| Lenders (Banks, Credit Unions) | Provide financing | DSCR, LTV, Debt Yield, borrower credit | Ensures the loan will be repaid safely |

| Investors | Purchase the property | Cap rate, IRR, cash flow, appreciation potential | Determines whether the deal produces strong returns |

| Underwriters | Analyze financial data | Income, expenses, lease terms, market conditions | Confirms whether the deal is financially viable |

| Brokers | Facilitate transactions | Market comparables and pricing | Help buyers and lenders understand property value |

| Asset Managers | Oversee property performance | Operating costs, tenant stability | Ensure the property maintains a healthy income |

The main professionals involved in CRE underwriting and the financial factors each group evaluates when analyzing a commercial property deal.

As Blooma.ai explains in their guide to CRE underwriting, underwriting is a critical safeguard for lenders, investors, and everyone involved in a commercial real estate deal. It is not a formality. It is the foundation of every smart decision in this industry.

Who Does CRE Underwriting and What Are They Looking For

Two main groups do commercial real estate underwriting. The first group is lenders. The second group is investors. They both study the same property. But they look at it from different angles.

Lenders are banks, credit unions, and debt funds. They lend money to buy properties. Their job is to make sure they get paid back. So they focus on risk. They ask: if I lend $5 million on this building, will the property’s income cover the loan payments? What happens if things go wrong? They look at the borrower’s credit, the property’s cash flow, and how much of the value is covered by the loan.

Investors are the people or companies buying the property. They focus on return and ask: if I put my money into this deal, what do I get back? They care about the income the property produces, how much it might grow, and how much they can sell it for later.

According to Agora Real’s comprehensive CRE underwriting guide, both groups look at the same key areas: the property’s income potential, location, tenants, operating costs, market conditions, and how the deal is financed. These are the building blocks of every underwriting analysis.

Key Stat: As of June 2025, only 9% of banks are tightening their CRE lending standards — down from 67.4% in April 2023. This means it is easier to get a CRE loan today than it has been in years. Understanding underwriting helps you take advantage of this window. — Federal Reserve Senior Loan Officer Survey, 2025

The Difference Between Lender Underwriting and Investor Underwriting

Lenders and investors both underwrite the same deal. But their goals are very different. Knowing this difference helps you prepare better — whether you are asking for a loan or evaluating a purchase. Lender underwriting is careful and conservative. The lender is not trying to make big profits from the property. They just want their loan paid back safely. So they focus on the worst case. What happens if the property loses some tenants and rents go down? What if the borrower runs into trouble? They want to know the deal still works even when things are not perfect.

Investor underwriting is more focused on opportunity. The investor wants to know: Does the upside justify the risk? They look at the property over a full holding period — usually 5 to 10 years. They model different outcomes. Best case, normal case, and worst case. They care about total return, not just monthly cash flow.

For a clear visual walkthrough of how lenders look at a real CRE deal step by step, this YouTube tutorial on CRE underwriting is a great companion to this written guide. It shows real deal math in action.

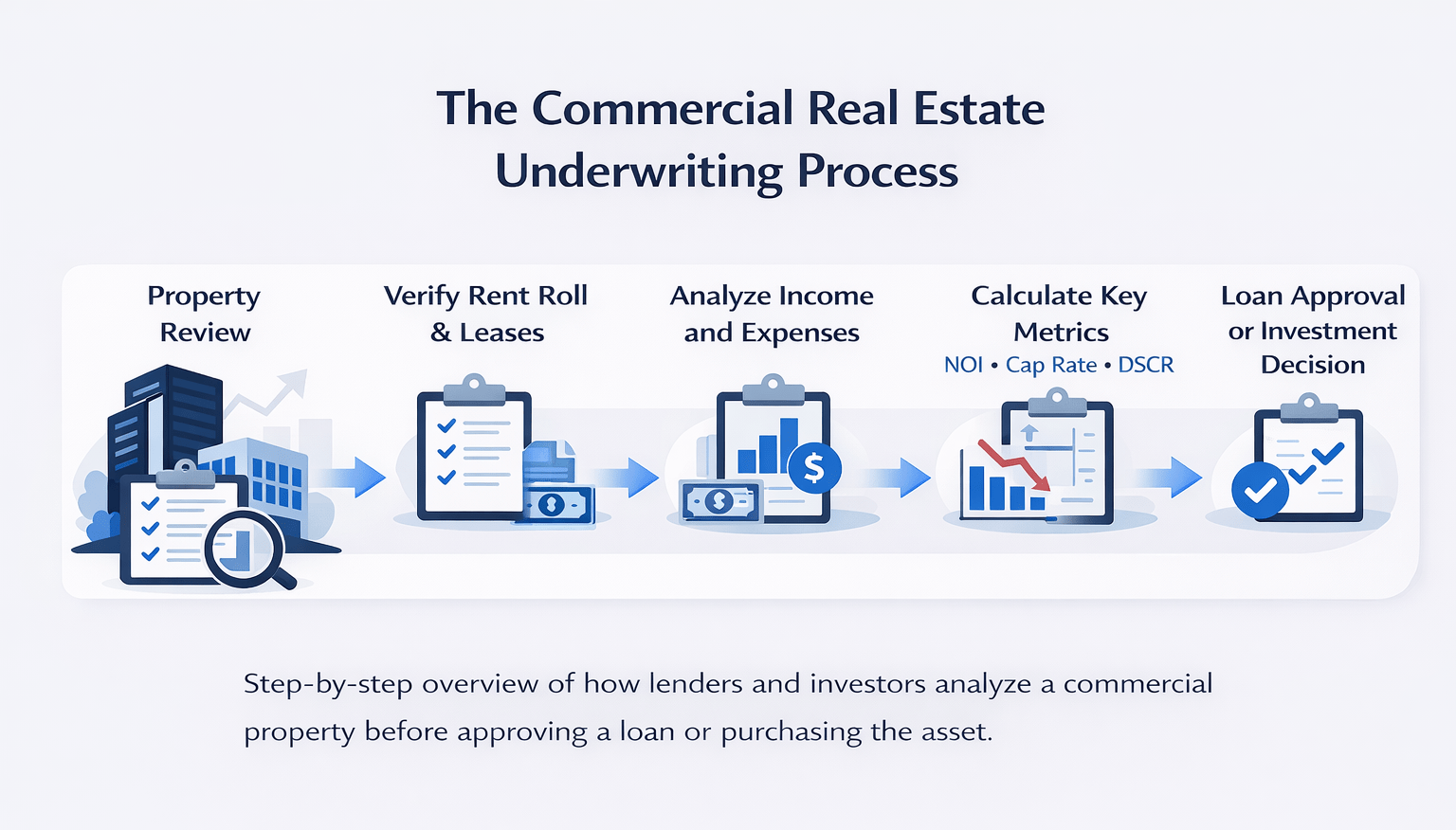

The Commercial Real Estate Underwriting Process Step-by-Step

Step 1 — Study the Property and Check the Basic Facts

Review the Seller’s Documents

Every underwriting process starts with the same first step. You need to understand exactly what you are buying or lending on. Before you look at a single number, you need to know the facts on the ground. This is called preliminary due diligence — but think of it simply as doing your homework.

Here is what you check in this first step:

- Look at the offering documents: The seller gives you a package of information. This includes rent rolls, income statements, and lease summaries. Read all of it carefully. These documents give you a starting picture — but you need to verify everything

- Check the location: Is the building easy to get to? Is it close to things that drive demand — employers, highways, transit, shopping? Is the neighborhood improving or declining? Location affects how easy it will be to keep the building full

- Check the physical condition: Walk the building. Look for problems. A roof that needs replacing, old HVAC equipment, or outdated plumbing all cost money. These costs come out of your returns

- Check the legal status: Is the property zoned correctly for its use? Are there any lawsuits, title problems, or environmental issues? These can delay or kill a deal

- Study the tenants: Who is renting the space? Are they financially strong? When do their leases end? A building with leases ending in 12 months is much riskier than one with 5-year leases still running

Here is a real example. You are looking at a 50,000 sq ft office building in Nashville. The seller says the building is 90% full and earns $800,000 per year. Your job at this stage is to verify that. Are the leases real and current? Do any big tenants leave soon? Are some tenants on short monthly agreements? Is there a long maintenance to-do list? The answers change everything.

As Security Bank and Trust’s CRE underwriting guide explains, reviewing lease agreements, their end dates, and how likely tenants are to renew is one of the most important steps in checking a property’s future income stability.

Step 2 — Build the Financial Model and Calculate the Key Numbers

Once you know the facts about the property, the next step is to run the numbers. This is the heart of underwriting. You build a financial model that shows what the property truly earns — and what it costs to run. All the key metrics — the ones lenders care about most — come from this model.

Here is how the model is built from top to bottom:

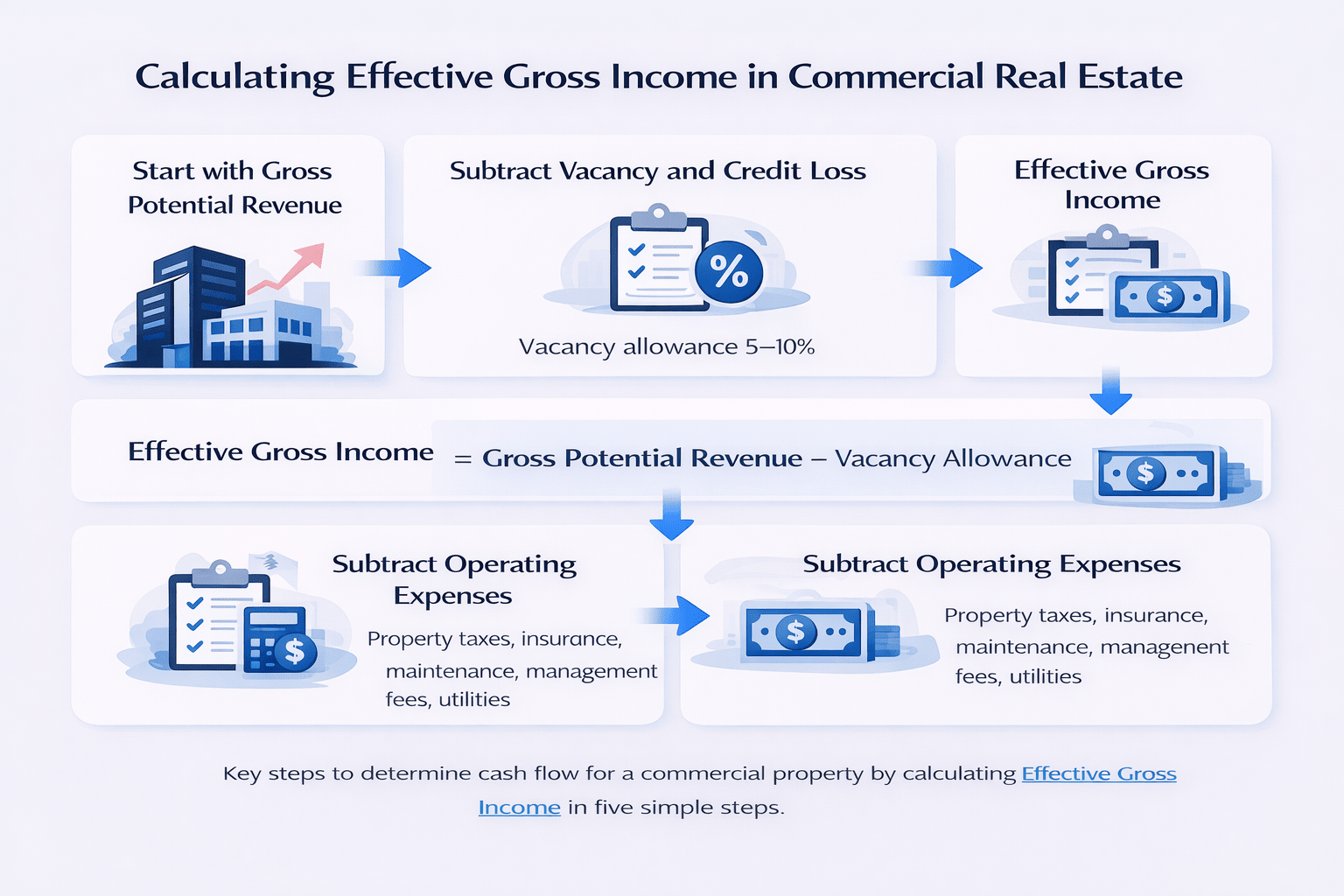

Start with Gross Potential Revenue:

This is the total income the building would earn if every space were rented at the full market rate. It is the highest possible number. You always work down from here.

Subtract Vacancy and Credit Loss: (Effective Gross Income = Gross Potential Revenue minus Vacancy Allowance)

No building is ever 100% full all the time. Most underwriters use a 5% to 10% vacancy allowance based on local market data.

Subtract Operating Expenses: (NOI = Effective Gross Income minus Total Operating Expenses)

This includes property taxes, insurance, management fees, maintenance, and utility costs if the owner pays them.

Calculate Cash Flow to the Owner: (Cash Flow = NOI minus Annual Loan Payments)

Here is the Nashville example in action. The building has a Gross Potential Revenue of $800,000. With a 7% vacancy allowance, the effective gross income is $744,000. Operating expenses total $280,000. NOI is $464,000. If annual loan payments are $360,000, the owner’s cash flow is $104,000. That is the real income left after all costs and debt.

For a deeper look at how lenders verify and normalize NOI from real income data, Avana Capital’s guide to the CRE underwriting process walks through the lender’s exact approach to income checking with plain examples.

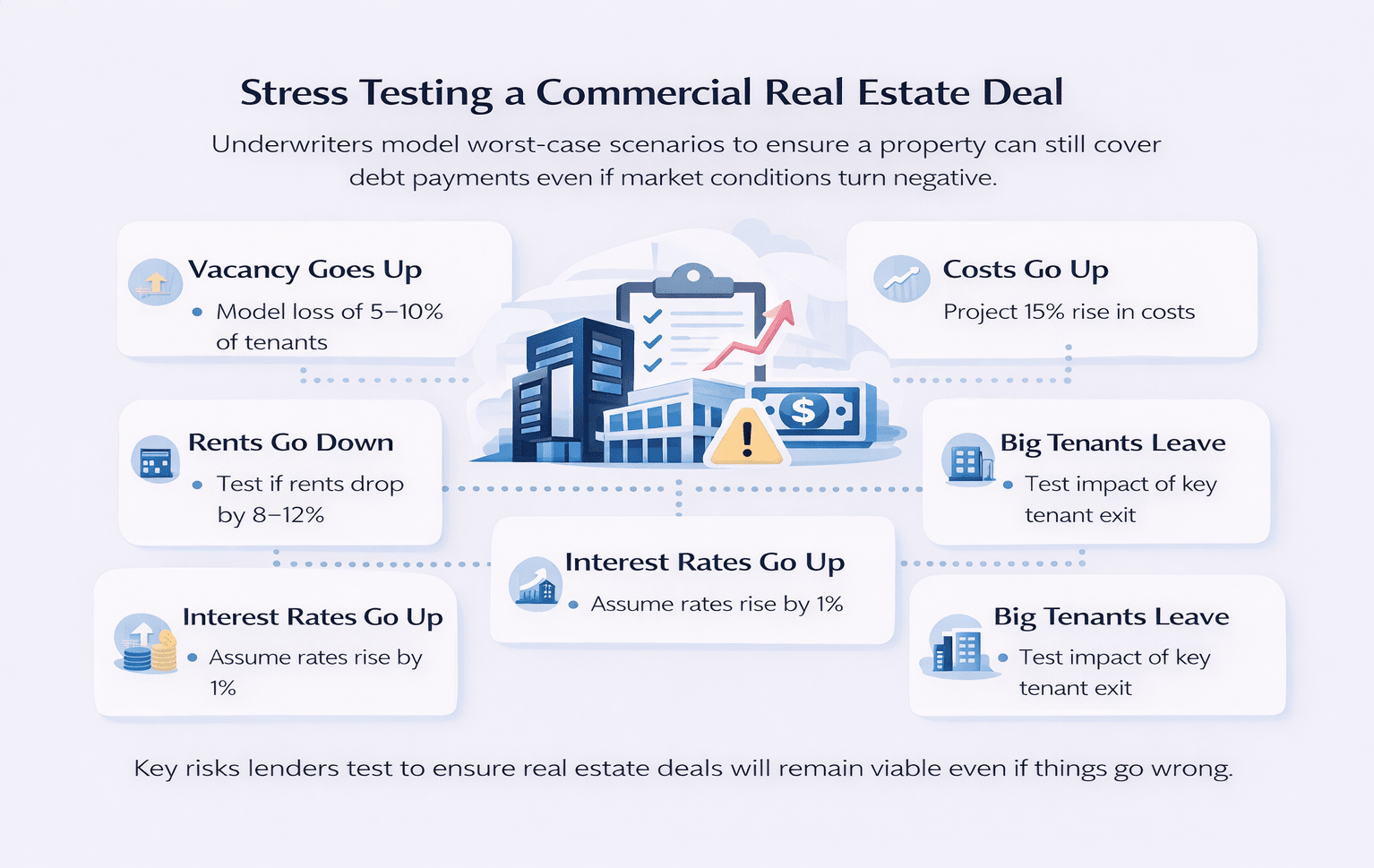

Step 3 — Test the Deal Against Worst-Case Scenarios

Building a financial model shows what the deal looks like today. But underwriting does not stop there. You also need to test what happens when things go wrong. This is called stress testing. It is one of the most important steps — and one that many new investors skip.

Here are the key risks every underwriter tests:

- Vacancy goes up: What happens if the building loses 5% to 10% more tenants than expected? Does it still cover the loan payments? Run the numbers both ways

- Rents go down: What if the market softens and rents drop 8% to 12%? How does that affect NOI and DSCR?

- Interest rates go up: If you have a floating-rate loan, what happens if rates rise by 1%? A 1% rate increase on a $10 million loan adds $100,000 to annual debt payments

- Costs go up: What if operating costs rise 15% due to higher taxes or insurance? Does the deal still work?

- Big tenants leave: What percentage of income comes from just one or two tenants? What happens if they do not renew their leases?

Key Insight: A deal that only works when everything goes perfectly is a risky deal. A deal that still covers its loan payments even when vacancy rises 10% is a deal worth doing. Stress testing shows you which one you are looking at.

Market Data: The average LTV across new CMBS loans in 2024 was 54.9%, with an average DSCR of about 1.40x. This shows lenders are requiring real equity and strong cash flow before they approve loans in today’s market. — CRED iQ CMBS Underwriting Trends Report, October 2024

The Seven Key Numbers Every CRE Underwriter Must Understand

Why These Seven Metrics Matter in CRE Underwriting

Seven numbers form the backbone of commercial real estate underwriting. Every deal, every lender, and every investor refers to some or all of these. The table below puts all seven in one place so you can see exactly what each one measures, how to calculate it, and what a healthy number looks like.

| Metric | Simple Formula | What It Checks | What Lenders Want | Why It Matters |

| NOI | Gross Income minus Operating Costs | How much the property earns after running costs | The higher the better | Every other calculation starts here |

| Cap Rate | NOI divided by Property Value x 100 | The return rate compared to what you paid | 5% to 8% is typical | Let’s you compare two different properties quickly |

| DSCR | NOI divided by Annual Loan Payments | Can the property pay back the loan each year? | At least 1.20x to 1.25x | The most important number for loan approval |

| LTV | Loan Amount divided by Property Value x 100 | How much of the property is paid for with the loan? | 60% to 75% is normal | Shows how much equity the borrower has |

| Debt Yield | NOI divided by Loan Amount x 100 | What the lender earns if they take the property back | At least 8% to 10% | A clean risk check that does not change with interest rates |

| IRR | Total return over the full holding period | How much does the whole deal return over time? | Usually 12% to 20% or more | The main number investors use to judge a deal |

| OER | Operating Costs divided by Gross Income x 100 | How well is the property managed day to day? | Below 40% to 50% is healthy | A rising OER is a warning sign |

Now, let us walk through the three most important ones with real calculations. These are the ones every lender checks first — and every investor should know cold.

NOI, Cap Rate, and DSCR — The Three Numbers That Drive Every Decision

These three numbers come up in every single CRE deal. Learn these well, and you will be able to analyze any property quickly and with confidence.

Example Commercial Real Estate Underwriting Calculation

| Metric | Formula | Example Numbers | Result |

|---|---|---|---|

| Gross Potential Revenue | Total rent if fully occupied | $800,000 | $800,000 |

| Vacancy Allowance (7%) | Revenue × vacancy rate | $800,000 × 7% | $56,000 |

| Effective Gross Income | Revenue − vacancy | $800,000 − $56,000 | $744,000 |

| Operating Expenses | Taxes, insurance, maintenance | $280,000 | $280,000 |

| Net Operating Income (NOI) | EGI − Expenses | $744,000 − $280,000 | $464,000 |

| Annual Loan Payments | Debt service | $360,000 | $360,000 |

| Cash Flow | NOI − Debt Payments | $464,000 − $360,000 | $104,000 |

A simplified example showing how underwriters move from potential income to final cash flow using common CRE financial metrics.

Understanding Net Operating Income (NOI)

NOI is the starting point for everything. It tells you what the property earns after all running costs, but before loan payments. Every other calculation in underwriting flows from this number.

NOI = Effective Gross Income minus Operating Expenses

Example: A retail strip center earns $620,000 in effective gross income. Operating costs are $190,000. NOI = $430,000. This is the number both the lender and the investor work from.

How Cap Rate Helps Compare CRE Investments

The cap rate tells you the return rate on the property based on its income and price. It lets you compare two different properties side by side in seconds.

Cap Rate = NOI divided by Property Value x 100

Example: NOI of $430,000 on a $6,000,000 property gives a cap rate of 7.2%. A lower cap rate (4% to 5%) usually means a safer, more expensive market. A higher cap rate (8% to 10%) usually means more risk or more return potential.

Why DSCR Matters to Commercial Lenders

DSCR is the most important number for lenders. It answers one question: can the property’s income cover the loan payments? If the answer is no, the loan does not get approved.

DSCR = NOI divided by Annual Loan Payments

Example: NOI of $430,000 divided by annual loan payments of $320,000 gives a DSCR of 1.34x. Most lenders need at least 1.20x to 1.25x. At 1.34x, this property passes. A DSCR below 1.00x means the property cannot pay its own debt — a clear red flag.

For a full breakdown of how lenders use DSCR to decide the maximum loan amount they will approve, Blooma.ai’s CRE underwriting explainer walks through the logic clearly with real deal examples.

LTV, Debt Yield, IRR, and OER — The Four Supporting Numbers

The first three metrics — NOI, Cap Rate, and DSCR — are the most important. But these four supporting numbers give you a fuller picture of the deal. Each one adds a different layer of information that helps lenders and investors make better decisions.

Loan-to-Value (LTV): Measuring Borrower Equity

LTV tells you how much of the property’s value is covered by the loan. The lower the LTV, the more equity the borrower has — and the safer the deal is for the lender.

LTV = Loan Amount divided by Property Value x 100

Example: A $4,500,000 loan on a $6,000,000 property gives an LTV of 75%. Most lenders cap LTV between 65% and 75%. In 2024, the average CMBS loan had an LTV of just 54.9% — showing how cautious lenders have been.

Debt Yield: A Rate-Independent Risk Metric

Debt yield is a risk check that does not change when interest rates change. It shows what return the lender would get if they had to take the property back today.

Debt Yield = NOI divided by Loan Amount x 100

Example: NOI of $430,000 on a $4,500,000 loan gives a debt yield of 9.6%. Most lenders need at least 8% to 10%. At 9.6%, this deal passes.

Internal Rate of Return (IRR) for CRE Investments

IRR measures the total return over the full life of an investment. It accounts for the money you put in, the income you receive each year, and what you sell the property for at the end. Investors use IRR to compare deals across different time periods and sizes.

Most investors target an IRR of 12% to 20% or more. Low-risk deals target 10% to 12%. Value-add deals target 15% to 20%. High-risk development deals target 20% to 25% or more.

Operating Expense Ratio (OER): Property Efficiency

OER tells you how efficiently the property is managed. It compares total operating costs to gross income.

OER = Operating Expenses divided by Gross Income x 100

An OER below 40% to 50% is generally healthy. A rising OER over time is a warning sign. It could mean the property is being poorly managed or that deferred repairs are starting to catch up.

For a detailed look at all seven metrics and how they work together in a full underwriting model, Agora Real’s CRE underwriting resource is one of the most complete and practical guides available online.

How to Prepare for CRE Underwriting and Avoid Common Mistakes

What You Need to Prepare Before the Underwriting Process Starts

Strong underwriting starts with strong preparation. Whether you are going to a lender for a loan or running your own analysis as an investor, the quality of your inputs decides the quality of your conclusions. Weak data leads to wrong decisions. Lenders can spot missing or questionable information very quickly.

Here is what you need to have ready before you start:

- Current rent roll: A full list of every tenant, their lease start and end dates, monthly rent, and any special deals or rent reductions. This is your income foundation

- 12 to 24 months of operating statements: Real income and expense records backed up by bank statements and receipts. Not just what the seller says — actual verified numbers

- Property tax bills: The real bills, not estimates. Property taxes often jump significantly when a property changes hands

- Insurance documents: Current coverage records and estimated replacement cost

- Capital expenditure history: What has been spent on repairs and upgrades in the past 3 to 5 years? What work still needs to be done?

- Personal financial statement: Most lenders want to see that the borrower has liquid money — usually 10% to 20% of the loan amount — sitting in the bank after the deal closes

- Entity and credit documents: Business formation papers, credit history, and records of past CRE experience all help the lender feel confident in the borrower

One of the biggest mistakes new CRE borrowers make is submitting projected numbers instead of real ones. Lenders do not underwrite based on what a property might earn someday. They underwrite based on what it actually earns today. Always submit verified historical data — not the seller’s optimistic projections.

Essential Documents Required for CRE Underwriting

| Document | What It Shows | Why Lenders Need It |

|---|---|---|

| Rent Roll | Tenant list, rents, lease terms | Confirms property income stability |

| Operating Statements (12–24 months) | Real income and expenses | Verifies financial performance |

| Property Tax Records | Current tax obligations | Helps estimate future expenses |

| Insurance Policies | Property coverage details | Ensures adequate risk protection |

| Capital Expenditure History | Repairs and upgrades | Shows property maintenance history |

| Borrower Financial Statement | Liquidity and assets | Confirms borrower’s financial strength |

| Entity Documents | Ownership structure | Verifies legal ownership and liability structure |

Key financial and property documents that lenders and investors review to verify income, expenses, ownership structure, and the borrower’s financial strength.

For a full checklist of what lenders review during the underwriting process, Security Bank and Trust’s CRE underwriting guide gives a clear, borrower-friendly breakdown of every document category you need to prepare.

The Most Common CRE Underwriting Mistakes and How to Fix Each One

Most deals that fail underwriting do not fail because the property is bad. They fail because the analysis was rushed, the numbers were too optimistic, or the borrower was not prepared. Here are the most common mistakes — and how to avoid each one.

- Using the seller’s projected income instead of real income: Sellers show their best case. Lenders underwrite to actual verified income. Always normalize the numbers to what the property has truly earned — not what it could earn in a perfect scenario

- Understating operating costs: First-time investors often underestimate property taxes, management fees, insurance, and capital reserves. Build in a 10% to 15% cost cushion above current actuals to be safe

- Ignoring when leases end: A property where 70% of leases expire in the next 18 months is a very different risk than one with 5-year leases still running. Always calculate the Weighted Average Lease Term — called WALT — before presenting a deal

- Borrowing too much: High debt makes returns look bigger in good times — but it makes losses much worse in bad times. The average CMBS LTV in 2024 was 54.9%. Match your debt level to what the market and the property can safely support

- Skipping the stress test: Always model what happens if vacancy goes up 10% or interest rates rise by 1%. If the deal falls apart under those conditions, it is too fragile to pursue

Market Insight: New CRE loan volume in early 2025 rose by over 90% year-over-year. Commercial mortgage spreads tightened by 183 basis points. Well-prepared borrowers with clean underwriting are winning the best loan terms in this recovering market. — Deloitte CRE Outlook 2026

How AI Is Making CRE Underwriting Faster and More Accurate

Underwriting used to take days. Analysts would spend hours building spreadsheets, checking income statements, running sensitivity tables, and formatting reports. AI is changing that — and the change is happening fast across the CRE industry.

Where AI Is Used in CRE Underwriting Today

Here is how AI tools are being used in underwriting right now:

- Document reading and data extraction: AI reads rent rolls, lease documents, and income statements and pulls out the key numbers automatically. What used to take 2 to 3 hours takes seconds

- Financial model building: AI tools can build a fully populated underwriting model from raw data — including NOI, DSCR, LTV, and sensitivity tables — with very little manual input

- Live market data: AI platforms pull in current vacancy rates, comparable rents, and cap rate trends from the market and use them to check your assumptions in real time

- Risk alerts: AI flags unusual patterns in the data — a sudden jump in expenses, rents that are well below market, or one tenant making up 60% of all income — and brings them to the analyst’s attention

- Speed: A full underwriting analysis that used to take 2 to 5 days can now be done in a few hours with AI-assisted tools

For CRE professionals who want to learn how to use AI tools in their underwriting and deal analysis workflow, building this skill is no longer optional. It is a real competitive advantage. The analysts and investors who use AI to move faster and take more risk will consistently outperform those who do not.

The AI for CRE Collective is a community of 600+ commercial real estate professionals who share tested AI workflows, prompt libraries, and practical tools built for CRE underwriting, acquisitions, and asset management. It is the most focused resource available for anyone who wants to start using AI in their CRE work — and see results on real deals.

Final Thoughts: CRE Underwriting Is a Skill That Pays for Itself

Commercial real estate underwriting is not just something lenders do. It is a skill that every investor, broker, developer, and analyst needs. It is how you know if a deal is worth doing before you commit your money or your reputation to it. Understanding NOI, cap rates, DSCR, LTV, and debt yield does not just help you pass a lender’s review. It helps you spot the good deals faster and walk away from the bad ones with confidence.

The process is learnable. The math is simple once you understand the logic. Start with one deal. Build the model. Run the numbers. Test the worst case. That process — repeated on deal after deal — is what separates investors who build real wealth from those who guess and hope. The CRE market is recovering fast. New loan volume is up over 90% year-over-year. Lenders are loosening standards. More deals are getting done. The investors who understand underwriting right now are the ones who will capture the best opportunities in this window.

Keep Learning With the AI for CRE Collective

Underwriting is just one part of what great CRE professionals do. The AI for CRE Collective is a group of 600+ real estate professionals. They share AI tools, prompts, and strategies that actually work on real buildings and deals. When you join, you get a Top 50 Prompt Library on Day 1. You also get weekly live Q&A calls and step-by-step workflows built for brokers, analysts, investors, and developers.

Prefer to start free? Subscribe to The Vertical — our free weekly newsletter covering the latest AI tools and workflows built for CRE professionals.

Join the AI for CRE Collective on Skool →

Subscribe to The Vertical — Free Weekly Newsletter →

The gap between CRE professionals who know how to underwrite well and those who are still figuring it out grows with every deal. Come close it inside the Collective.

FAQs About Commercial Real Estate Underwriting Explained

What is commercial real estate underwriting?

Commercial real estate underwriting is the process of checking a property’s numbers before money changes hands.

It is how lenders decide whether to give a loan. It is also how investors decide whether to buy a property. Here is what it covers:

- It checks how much money the property earns

- It checks how much it costs to run the property

- It checks how much debt the property can safely carry

- It looks at the borrower’s financial history and credit

- It tests what happens if things go wrong — like tenants leaving or rents going down

Think of it like a health check for a building. A doctor checks your test results before saying you are healthy. An underwriter checks a property’s numbers before saying the deal is safe.

Blooma.ai’s guide to CRE underwriting explains how underwriting protects lenders, investors, and everyone involved in a commercial real estate deal.

Underwriting turns a gut feeling into a fact-based decision — and that is what separates good deals from bad ones.

Why is commercial real estate underwriting important?

CRE underwriting is important because it stops you from making expensive mistakes with your money.

Without underwriting, you are guessing.

Here is why that is dangerous:

- You might overpay for a property that earns less than the seller claims

- You might borrow too much and not have enough cash flow to cover loan payments

- You might miss hidden costs that eat into your returns

- You might buy a property where big tenants are about to leave

- You might invest in a deal that only works in the best case, not in the real world

A real example: a seller tells you a building earns $600,000 per year. Underwriting checks the actual leases and real expense records. Maybe the true income is only $480,000. That difference changes everything about the deal.

Agora Real’s comprehensive CRE underwriting guide explains why underwriting is the foundation of every smart commercial real estate decision.

Underwriting does not slow a deal down — it saves you from the ones that would have cost you everything.

What is NOI, and why does it matter in CRE underwriting?

NOI stands for Net Operating Income. It is the single most important number in CRE underwriting.

Here is what you need to know about it:

- NOI tells you what a property earns after all running costs, but before loan payments

- The formula is simple: NOI = Effective Gross Income minus Operating Expenses

- Operating expenses include property taxes, insurance, management fees, and maintenance costs

- Loan payments are NOT included in the calculation — NOI is a pre-debt number

- Every other key metric in underwriting — cap rate, DSCR, debt yield — starts with NOI

Here is a simple example. A retail strip center earns $620,000 in effective gross income. Operating costs are $190,000. NOI = $430,000. That $430,000 is what both the lender and the investor use to run every other calculation.

Avana Capital’s guide to the CRE underwriting process explains how lenders verify and check NOI from real income data before approving any commercial loan.

Get the NOI wrong, and every other number in your underwriting model will be wrong too.

What is DSCR, and what number do lenders want to see?

DSCR stands for Debt Service Coverage Ratio. It is the number lenders care about most when reviewing a loan application.

Here is what it means and what the numbers look like:

- DSCR tells you whether the property’s income can cover its loan payments

- The formula is: DSCR = NOI divided by Annual Loan Payments

- A DSCR of 1.00x means the property just barely covers the loan — no cushion at all

- Below 1.00x means the property cannot cover its own debt — a clear red flag for any lender

- Most lenders need at least 1.20x to 1.25x before they will approve a loan

- A DSCR of 1.34x and above is considered healthy and comfortable for most lenders

Here is a simple example. NOI is $430,000. Annual loan payments are $320,000. DSCR = 1.34x. That passes most lenders’ minimum standard.

Blooma.ai’s CRE underwriting explainer walks through how lenders use DSCR to figure out the maximum loan amount they will approve on any property.

A DSCR below 1.25x will stop most loan applications before they even get reviewed — always calculate it before approaching a lender.

What is a cap rate in commercial real estate?

A cap rate — short for capitalization rate — shows the rate of return on a commercial property based on its income and its price.

Here is what you need to know:

- The formula is: Cap Rate = NOI divided by Property Value multiplied by 100

- A cap rate of 7.2% means the property earns 7.2 cents for every dollar of value

- Lower cap rates (4% to 5%) mean lower risk and higher prices — common in big city markets

- Mid-range cap rates (6% to 7%) are typical for stable properties in mid-size markets

- Higher cap rates (8% to 10%) usually mean more risk or more return potential — common in smaller markets

- Cap rates and property values move in opposite directions — when values go up, cap rates go down

Here is a quick example. A property with an NOI of $430,000 priced at $6,000,000 has a cap rate of 7.2%.

Agora Real’s CRE underwriting guide explains how cap rates change by property type, location, and market cycle with real examples.

Cap rate tells you the return you are getting at the price you are paying — always compare it to other similar properties before making an offer.

What is LTV in commercial real estate underwriting?

LTV stands for Loan-to-Value. It tells you how much of the property’s price is being paid by the loan.

Here is what lenders look at:

- The formula is: LTV = Loan Amount divided by Property Value multiplied by 100

- Most commercial lenders cap LTV between 65% and 75%

- In 2024, the average CMBS loan had an LTV of just 54.9% — showing that lenders are requiring real equity

- A higher LTV means more risk for the lender and less cushion for the borrower

- A lower LTV means the borrower has more equity in the deal — lenders see this as safer

- LTV is one of three tests lenders use to figure out the maximum loan size they will offer

Here is a quick example. A $4,500,000 loan on a $6,000,000 property gives an LTV of 75%. That is at the top of what most commercial lenders allow.

Security Bank and Trust’s CRE underwriting guide explains how LTV works alongside DSCR in the loan approval process for commercial properties.

The lower your LTV, the stronger your loan application — more equity means less risk for everyone in the deal.

What is debt yield, and why do lenders use it?

Debt yield is a risk check that lenders use to measure how safe a loan is — and it does not change when interest rates change.

Here is what makes it useful:

- The formula is: Debt Yield = NOI divided by Loan Amount multiplied by 100

- Unlike DSCR, debt yield is not affected by interest rates or the length of the loan

- This makes it a more consistent way to measure risk when rates are moving up or down

- Most lenders need a minimum debt yield of 8% to 10%

- It became widely used after the 2008 financial crisis, when low interest rates were making DSCR look better than it really was

- CMBS lenders in particular rely on debt yield as one of their main underwriting tests

Here is a simple example. NOI of $430,000 on a $4,500,000 loan gives a debt yield of 9.6%. That passes the typical 8% to 10% minimum.

Agora Real’s CRE underwriting resource covers how debt yield works alongside DSCR and LTV when lenders size the maximum loan they will approve on a deal.

Debt yield is the lender’s backup test — it keeps loan amounts grounded no matter what interest rates are doing.

What documents do I need for CRE underwriting?

Strong underwriting starts with strong documents — and lenders spot missing or weak paperwork fast.

Here is what you need to prepare before you start:

- Current rent roll: A full list of every tenant, their lease dates, monthly rent, and any special deals or rent reductions

- 12 to 24 months of operating statements: Real income and expense records backed up by actual bank statements — not just what the seller says

- Property tax bills: The real bills, not estimates. Taxes often jump significantly when a property is sold

- Insurance documents: Current coverage records and estimated replacement cost

- Capital expenditure history: What has been spent on repairs in the past 3 to 5 years — and what work is still needed

- Personal financial statement: Most lenders want to see that you have liquid money equal to 10% to 20% of the loan amount after the deal closes

- Entity and credit documents: Business formation papers, credit history, and records of past CRE deals you have done

The most common mistake new borrowers make is submitting projected numbers instead of real ones. Lenders underwrite to actual verified income — not what the property might earn someday.

Security Bank and Trust’s CRE underwriting guide gives a full borrower-friendly checklist of every document lenders review before issuing a loan approval.

Have every document ready before you approach a lender — it signals professionalism and speeds up the entire approval process.

How long does commercial real estate underwriting take?

CRE underwriting timelines depend on the lender type, deal complexity, and how ready your documents are.

Here are realistic timelines by lender type:

- Community banks and credit unions: 3 to 6 weeks from complete application to a commitment letter

- Regional and national banks: 4 to 8 weeks, depending on deal size and internal credit committee schedules

- CMBS lenders: 60 to 90 days — longer process with more third-party reports required

- Debt funds and bridge lenders: 2 to 4 weeks — the fastest option for time-sensitive deals

- SBA 504 loans: 60 to 90 days, including SBA review on top of the lender’s process

What slows down underwriting the most:

- Missing or incomplete documents at the start

- Unclear ownership structure or entity history

- Environmental issues that need extra studies

- Appraisal delays or valuations that come in below expectations

Avana Capital’s CRE underwriting process guide covers what borrowers can do to keep the underwriting process moving without delays.

The fastest way to speed up underwriting is to have every document ready before the very first lender conversation.

What is stress testing in CRE underwriting?

Stress testing is checking what happens to a deal’s numbers when things go wrong — not just when everything goes perfectly.

Here is what underwriters test and why:

- Vacancy goes up: What if the building loses 5% to 10% more tenants? Does it still cover loan payments?

- Rents go down: What if market rents drop 8% to 12%? How does that change the NOI and DSCR?

- Interest rates rise: For floating-rate loans, what happens if rates go up by 1%? A 1% rise on a $10 million loan adds $100,000 to annual debt payments

- Costs go up: What if operating costs rise 15% because of higher taxes or insurance?

- Big tenants leave: What happens to income if the building’s largest tenant does not renew their lease?

A deal that only works in the best case is a risky deal. A deal that still covers its loan payments even when vacancy rises 10% is a deal worth doing.

Blooma.ai’s CRE underwriting explainer covers how lenders build stress scenarios into their models before approving any commercial loan.

Stress testing is not being pessimistic — it is being prepared for the market conditions that always show up eventually.

What is the difference between lender underwriting and investor underwriting?

Both lenders and investors underwrite the same deal — but they look at it from very different angles.

Here is how their focus areas differ:

- Lender focus: Keeping risk low. They care about DSCR, LTV, debt yield, and whether the borrower has a strong credit history

- Investor focus: Making a good return. They care about cap rate, IRR, cash-on-cash return, and how much equity they get back at the end

- Lender timeframe: The loan period — usually 5 to 10 years

- Investor timeframe: The full holding period — usually 5 to 10 years, with an exit sale at the end

- Lender’s worst case: Getting their loan paid back in full if the deal goes sideways

- Investor worst case: Not losing the equity they put into the deal

Both groups look at the same NOI number. But the lender asks, “Does this cover my loan?” while the investor asks, “Does this earn the return I need?”

Agora Real’s CRE underwriting guide explains how lender and investor underwriting models are set up differently in both structure and decision-making.

Understanding both sides makes you a better borrower and a smarter investor at the same time.

What is IRR, and how is it used in CRE underwriting?

IRR stands for Internal Rate of Return. It is the main number investors use to judge how good a deal is over the full time they hold it.

Here is what you need to know:

- IRR measures the total return across the whole holding period — not just the monthly cash flow

- It accounts for the money you put in, the income you earn each year, and what you sell the property for at the end

- Low-risk core deals: Target IRR of 10% to 12%

- Value-add deals: Target IRR of 15% to 20%

- High-risk development deals: Target IRR of 20% to 25% or more

- A higher IRR is better — but always look at the risk that comes with it, not just the number on its own

IRR can look great on paper if the model assumes aggressive rent growth or a very high sale price at exit. Always stress test your exit assumptions before trusting a high IRR number.

Avana Capital’s CRE underwriting process guide explains how IRR fits alongside cash-on-cash return and equity multiple in a full investor underwriting model.

IRR tells the full story of a deal’s return — but only if the assumptions that go into the model are honest ones.

What are the most common CRE underwriting mistakes?

Most deals that fail underwriting do not fail because the property is bad — they fail because the analysis was sloppy or too optimistic.

Here are the most common mistakes and the fix for each one:

- Using seller projections instead of real income: Always underwrite to actual verified income — not what the property might earn in a perfect world

- Understating operating costs: Add a 10% to 15% cushion above current actuals for taxes, insurance, and reserves

- Missing lease rollover risk: Always calculate the Weighted Average Lease Term — called WALT. Leases that are about to expire are the biggest source of income risk in most CRE deals

- Borrowing too much: High debt amplifies gains in good times and losses in bad ones. Match your debt level to what the property and the market can safely hold

- Skipping the stress test: Always model vacancy up 10% and interest rates up 1% before calling a deal done

- Submitting projections to lenders: Lenders check real historical performance — not future projections without backup evidence

Security Bank and Trust’s CRE underwriting guide covers how experienced lenders spot and respond to common underwriting errors in borrower submissions.

Fix these mistakes before they reach the lender, and your approval process will be faster and cleaner every time.

How does AI help with commercial real estate underwriting?

AI is making CRE underwriting faster, more accurate, and much less time-consuming for analysts and investors.

Here is how AI tools are being used in underwriting right now:

- Document reading: AI pulls rent roll data, lease terms, and financial numbers from PDF documents in seconds — no more hours of manual data entry

- Model building: AI tools build a full underwriting model from raw input data automatically — including NOI, DSCR, LTV, and sensitivity tables

- Live market data: AI platforms pull in current vacancy rates, comparable rents, and cap rate trends, and check your assumptions against the real market

- Risk alerts: AI flags unusual patterns — a big jump in expenses, rents well below market, or one tenant making up most of the income

- Speed: A full underwriting analysis that used to take 2 to 5 days can now be done in a few hours

What used to take a full analyst team several days can now be completed in hours with the right AI workflow.

The AI for CRE Collective is a community of 600+ CRE professionals who share tested AI underwriting workflows, prompt libraries, and deal analysis tools built for real commercial real estate work.

Learning to use AI in your underwriting process is no longer a nice-to-have — it is a real competitive advantage that grows with every deal you do.

How does a lender decide the maximum loan amount?

Lenders use three tests at the same time to figure out the biggest loan they can safely approve — and the lowest result of all three tests wins.

Here is how the three tests work:

- LTV test: Maximum loan = Property Value multiplied by Maximum LTV allowed (for example, 70%)

- DSCR test: Maximum loan = the loan amount at which NOI still achieves the minimum required DSCR (usually 1.25x)

- Debt Yield test: Maximum loan = NOI divided by the minimum required Debt Yield (usually 9.5%)

- The lender always picks the lowest number from all three tests

- This makes sure the loan is safe from every angle at the same time

Here is a real example. The LTV test gives a maximum loan of $4,200,000. The DSCR test gives $4,350,000. The Debt Yield test gives $4,526,000. The lender uses $4,200,000 — the lowest number wins.

Avana Capital’s guide to the CRE underwriting process walks through this maximum loan sizing process step by step with real deal numbers.

Knowing which test is limiting your loan tells you exactly what to improve to get approved for more.

What is the Operating Expense Ratio, and what does it show?

The Operating Expense Ratio — called OER — shows how well a commercial property is managed by comparing its costs to its income.

Here is what the numbers tell you:

- The formula is: OER = Operating Expenses divided by Gross Income multiplied by 100

- Below 35%: Very efficient — common in NNN lease properties where tenants pay most costs

- 35% to 50%: Healthy range for most commercial properties

- Above 50%: Could mean the property is being poorly managed, or costs are too high

- A rising OER over time is a warning sign — it usually means deferred repairs are piling up or management is losing control of costs

- Comparing OER to similar properties in the same market tells you whether your building is running well or not

Here is a quick example. A property with $190,000 in operating costs and $620,000 in gross income has an OER of 30.6%. That is efficient — common for a property with NNN leases where tenants handle most costs.

Blooma.ai’s CRE underwriting resource covers how lenders use OER alongside NOI to check the quality of a property’s management and financial records.

A healthy OER means a well-run property — a high or rising OER is a flag you need to investigate before closing.

What is lease rollover risk, and why does it matter?

Lease rollover risk is the risk that tenants will not renew when their leases end — and that the property will lose income as a result.

Here is why it matters so much in underwriting:

- A property where 70% of leases end in the next 18 months is much riskier than one with leases running for 7 more years

- WALT — Weighted Average Lease Term: The main metric for measuring this risk across all tenants in a building

- Lenders discount income from short leases because they want to see stability that lasts beyond the loan term

- Finding a new tenant costs money — you pay for improvements, leasing commissions, and lose rent during the empty period

- Office and retail properties carry the highest rollover risk because leases are long, and tenant decisions are slow

- Industrial and multifamily buildings have shorter but more predictable lease cycles — rollover is easier to manage

Security Bank and Trust’s CRE underwriting guide explains how lenders study lease expiration schedules and tenant renewal odds during the underwriting review process.

Always calculate your WALT before presenting a deal — lenders will ask, and a short WALT will lower the maximum loan amount they offer.

How do interest rates affect CRE underwriting?

Interest rates affect almost every debt-based number in CRE underwriting — and even small changes can make or break a deal.

Here is how the rate changes flow through the numbers:

- Rates go up, debt service goes up, DSCR goes down: A 1% rate increase on a $10 million loan adds about $100,000 to annual loan payments

- Higher rates mean smaller maximum loans: When DSCR drops below the lender’s minimum, the loan size has to shrink

- Higher rates push property values down: As cap rates rise with interest rates, property values fall, which also changes the LTV calculation

- Floating-rate loans carry the most risk: Always model a 1% to 2% rate increase in your stress test if you are using a floating-rate loan

- Fixed-rate loans protect cash flow: But they may come with early repayment penalties if you need to refinance before the loan term ends

In early 2025, commercial mortgage spreads tightened by 183 basis points. This means borrowing conditions improved significantly for well-prepared borrowers with clean underwriting.

Avana Capital’s CRE underwriting process guide covers how to build your underwriting assumptions correctly in different interest rate environments.

Always stress test your loan payments — rate changes are the fastest way for a deal that looked good to stop working.

What property types need different underwriting approaches?

Commercial real estate covers many different property types — and each one needs a slightly different underwriting focus.

Here is how underwriting changes by property type:

- Multifamily: Focus on occupancy trends, unit-by-unit rent rolls, and local rental supply coming to market

- Office: Focus heavily on lease rollover risk, how strong the tenants are financially, and WALT — vacancy in many office markets is still high after COVID

- Retail: Check tenant sales data for percentage rent leases, how strong the anchor tenants are, and foot traffic trends

- Industrial: Strong market right now — focus on clear height, dock door count, power supply, and distance to major highways and logistics routes

- Hotels: Underwrite on RevPAR (Revenue Per Available Room) and ADR (Average Daily Rate) instead of standard rent rolls

- New construction: Focus on feasibility, construction cost verification, and how fast the market can absorb new space

Agora Real’s CRE underwriting guide covers how underwriting changes across the major commercial property types with practical examples for each one.

The right underwriting approach depends on the asset — always adjust your model for the specific risks that come with the property type you are analyzing.

How do I get started with CRE underwriting today?

Getting started with CRE underwriting is simpler than most people think — you do not need a finance degree, just a clear process and the right tools.

Here is the simple starting sequence:

- Step 1 — Learn the seven core metrics: NOI, Cap Rate, DSCR, LTV, Debt Yield, IRR, and OER. These are the building blocks of every underwriting analysis

- Step 2 — Find one real deal: A local listing, an offering memorandum, or a case study. Build your first model in Excel or Google Sheets

- Step 3 — Use real operating statements: Practice with actual income and expense data — not seller projections

- Step 4 — Run all three loan sizing tests: LTV, DSCR, and Debt Yield. Find which one limits the deal

- Step 5 — Stress test your base case: Model vacancy up 10% and interest rates up 1%. See if the deal still works

- Step 6 — Watch a real deal walkthrough: This YouTube CRE underwriting tutorial is a great visual companion to the formulas in this guide

- Step 7 — Build your AI workflow: Start using AI tools to pull data, build models, and flag risks faster than you can manually

For analysts and investors who want to use AI to underwrite deals faster and analyze more properties in less time, AI for CRE Collective is a community of 600+ active CRE professionals sharing tested AI workflows, prompts, and strategies that work on real deals.

The best way to learn CRE underwriting is to build a model on a real deal today — every concept becomes simple the moment the numbers are in front of you.

References and Further Reading

-

- Agora Real — Commercial Real Estate Underwriting Guide: https://agorareal.com/learn/commercial-real-estate-underwriting/

- Blooma.ai — What Is Commercial Real Estate Underwriting: https://www.blooma.ai/blog/what-is-commercial-real-estate-underwriting

- Security Bank and Trust — CRE Underwriting for Investors: https://www.security-banks.com/blog/commercial-real-estate-underwriting

- Avana Capital — CRE Underwriting Process Guide: https://avanacapital.com/business-loans/commercial-real-estate-underwriting-process/

- YouTube — CRE Underwriting Tutorial: https://www.youtube.com/watch?v=UkZV8oCvWds

- AI for CRE Collective: https://aiforcrecollective.com