How We Use AI to Turn Raw Financials into Clean Underwriting Models

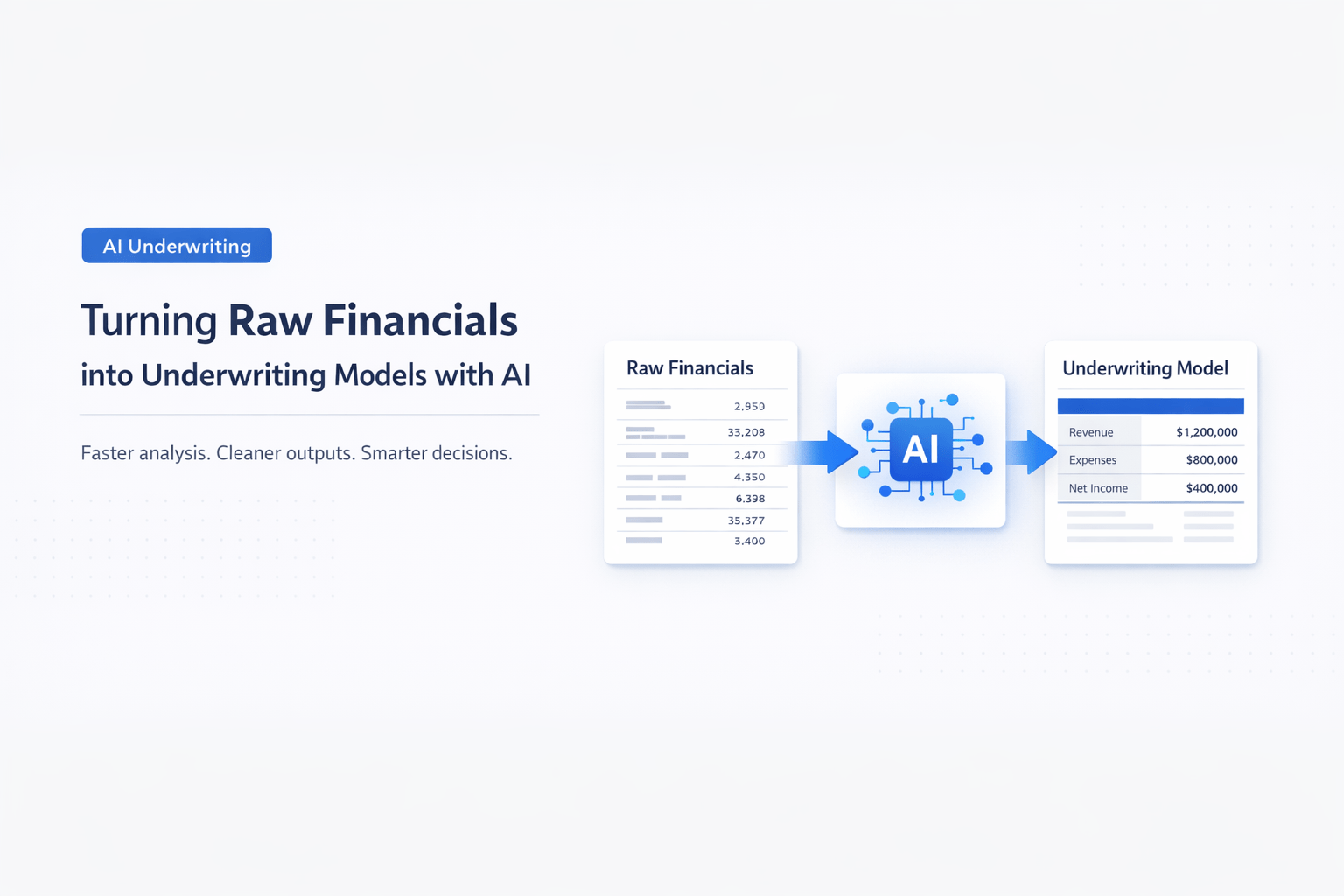

AI underwriting models in commercial real estate are changing how deals get analyzed. For years, underwriting has been slow, manual, and dependent on spreadsheets. Teams spend hours cleaning data before they even start modeling.

Now, that process is shifting. Instead of working through messy files line by line, AI underwriting models in commercial real estate help convert raw financials into structured, usable models within minutes. This change is not just about speed. It also improves consistency and reduces costly errors.

In most deals, financial data comes from different sources. You may get a rent roll in Excel, a T12 in PDF, and an offering memorandum with mixed formats. These files rarely match. So, analysts spend most of their time organizing data instead of analyzing it.

That is where AI makes a real difference. At its core, AI underwriting models in commercial real estate focus on one thing: turning unstructured data into clean, decision-ready outputs. This means fewer manual steps and faster deal evaluation.

At AI for CRE Collective, we focus on teaching professionals how to apply these systems in real workflows. Tools alone are not enough. The real value comes from knowing how to use them in underwriting.

The Traditional CRE Underwriting Process (And Why It Breaks at Scale)

Before AI underwriting models in commercial real estate became practical, underwriting followed a predictable but time-heavy process. It still does in many firms today.

What “Raw Financial Data” Actually Looks Like

Raw financial data in CRE is rarely clean. It comes in different formats and often lacks consistency.

Typical inputs include:

-

Rent rolls with inconsistent column names

-

T12 statements with missing categories

-

Lease documents in scanned PDFs

-

Broker offering memorandums with mixed data formats

In many cases, the same property will have different numbers across documents. That creates confusion early in the process.

Also, file formats create friction:

-

PDFs are hard to edit

-

Excel sheets may have broken formulas

-

Scanned documents require manual review

Because of this, teams spend more time preparing data than analyzing it.

Step-by-Step Manual Underwriting Workflow

The traditional workflow is detailed and repetitive. It usually follows these steps:

-

Data collection: Gather rent rolls, T12s, leases, and OMs

-

Data extraction: Manually pull numbers from documents

-

Data cleaning: Fix errors, align categories, remove duplicates

-

Model building: Enter data into Excel or underwriting software

-

Assumptions setup: Add growth rates, vacancy, and expense ratios

-

Analysis and output: Calculate NOI, IRR, and cash flows

Each step depends on the previous one. If errors occur early, they carry forward. If you want to understand how this process can be improved, this detailed breakdown of an AI acquisition underwriting workflow shows how each step can be streamlined.

Key Pain Points CRE Professionals Face

This process works for small deal volumes. But it breaks when the scale increases.

Common issues include:

-

Too much time spent on data cleaning

-

High risk of manual errors

-

Lack of standard formats across deals

-

Delays in decision-making

In practice:

-

Analysts often spend 60–70% of their time cleaning data

-

Teams struggle to evaluate multiple deals at once

-

Senior professionals rely on inconsistent outputs

Comparison: Manual vs AI-Based Underwriting Workflow

| Process Step | Manual Underwriting | AI Underwriting Models in Commercial Real Estate |

|---|---|---|

| Data Extraction | Manual entry from PDFs and Excel | Automated extraction from all file types |

| Data Cleaning | Time-consuming and error-prone | Automated standardization |

| Model Creation | Built manually in Excel | Generated instantly using AI |

| Error Detection | Requires manual review | AI flags inconsistencies automatically |

| Time per Deal | Several hours to days | Minutes to under an hour |

| Scalability | Limited by team size | Easily scalable across many deals |

This is where AI underwriting models in commercial real estate stand out. They remove repetitive steps and allow teams to focus on decision-making.

How AI is Changing Commercial Real Estate Underwriting

AI underwriting models in commercial real estate are not just improving speed. They are reshaping the entire workflow.

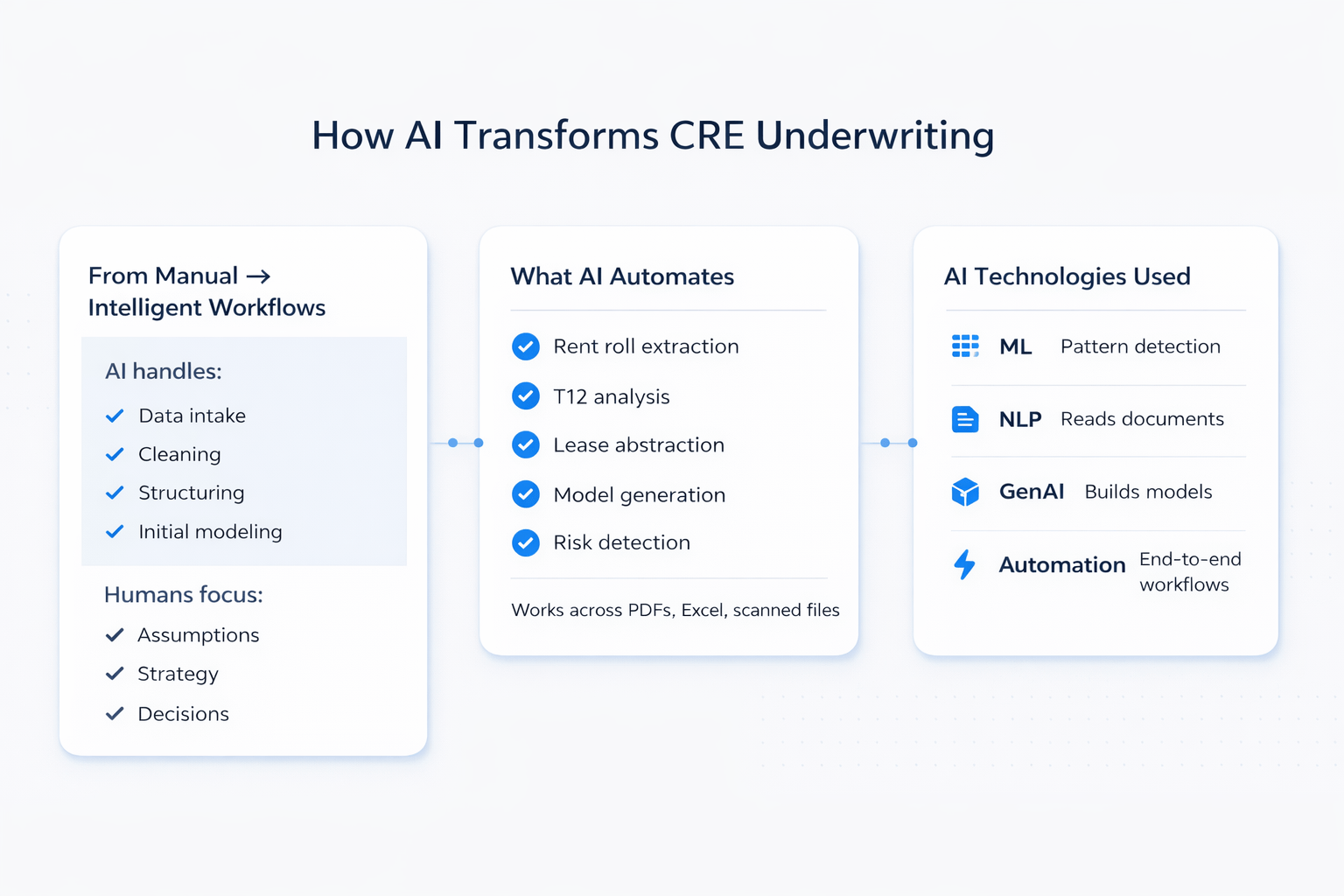

From Manual Models to Intelligent Workflows

In traditional underwriting, tools support the user. With AI, the workflow itself becomes automated.

Instead of asking, “How do I build this model?” The question becomes, “How do I review and adjust this model?”

This shift matters because it changes how teams operate.

AI handles:

-

Data intake

-

Cleaning

-

Structuring

-

Initial modeling

Humans focus on:

-

Assumptions

-

Strategy

-

Investment decisions

What AI Can Actually Automate in CRE

AI underwriting models in commercial real estate can handle several key tasks:

-

Rent roll extraction and structuring

-

T12 income and expense analysis

-

Lease abstraction from PDFs

-

Financial model generation

-

Risk flagging and anomaly detection

This removes the need for repetitive manual input.

Also, AI works across formats. It can process:

-

PDFs

-

Excel files

-

Scanned documents

-

Mixed data sources

Types of AI Used in Underwriting

Different types of AI work together in underwriting systems.

1. Machine Learning

-

Identifies patterns in financial data

-

Improves accuracy over time

2. Natural Language Processing (NLP)

-

Reads leases and documents

-

Extracts key terms and numbers

3. Generative AI

-

Builds financial models

-

Creates summaries and reports

4. Workflow Automation (Agent-Based Systems)

-

Connects multiple steps into one process

-

Runs end-to-end underwriting tasks

Together, these technologies power modern AI underwriting models in commercial real estate.

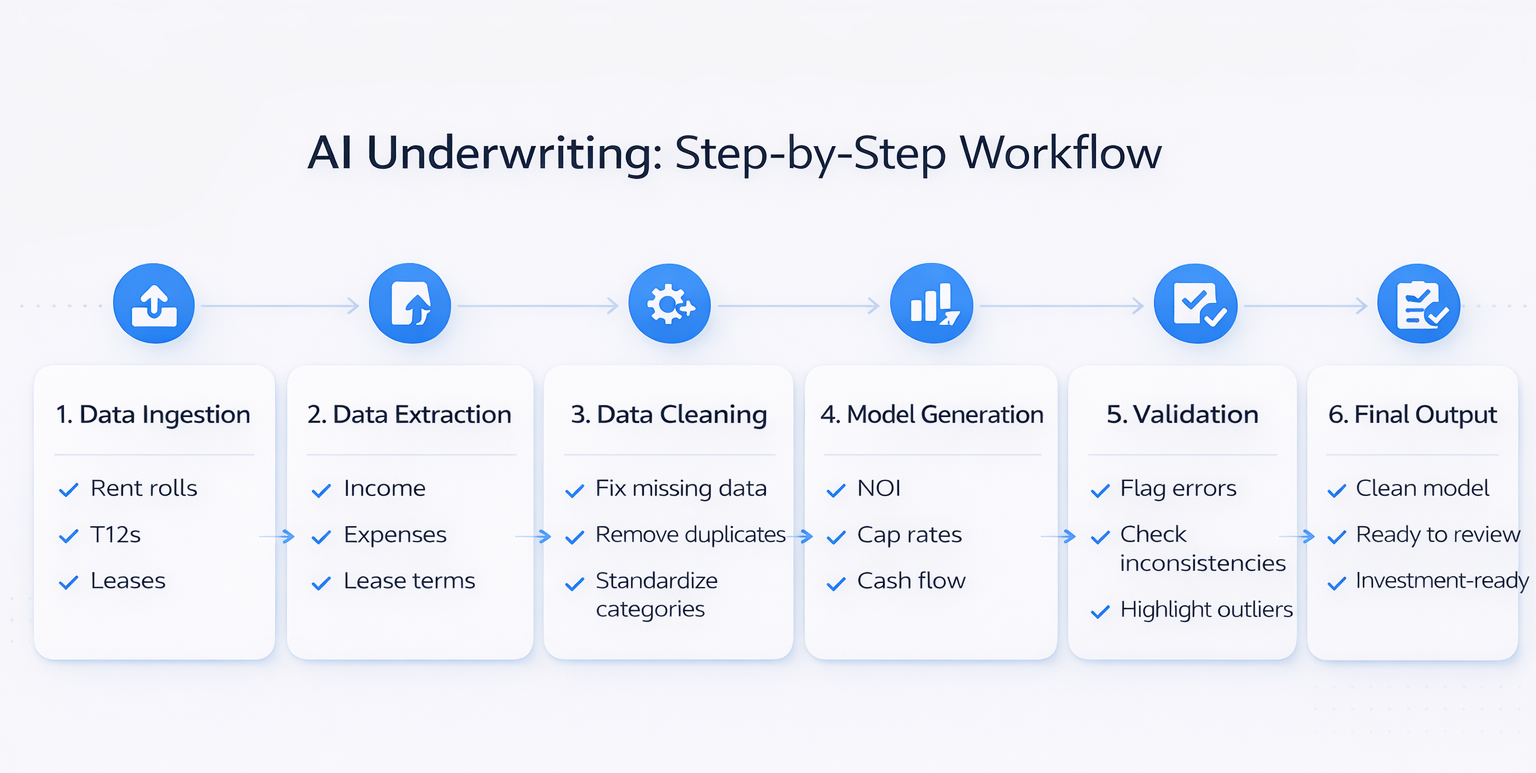

Step-by-Step: Turning Raw Financials into Clean Underwriting Models Using AI

To understand the real impact, it helps to look at the process step by step.

Step 1: Data Ingestion from Multiple Sources

The process starts with uploading documents.

These may include:

-

Rent rolls

-

T12 statements

-

Offering memorandums

-

Lease agreements

AI systems accept all formats. There is no need to convert files manually. This alone saves time at the start of underwriting.

Step 2: Automated Data Extraction

Once files are uploaded, AI begins extracting data.

It pulls key information such as:

-

Rental income

-

Operating expenses

-

Occupancy rates

-

Lease terms

The system reads both structured and unstructured data. This replaces hours of manual work.

Step 3: Data Cleaning and Standardization

Once the data is extracted, the next step is cleaning it. This is where most underwriting time is usually spent.

In manual workflows, analysts fix:

-

Missing values

-

Duplicate entries

-

Misaligned categories

-

Inconsistent naming (e.g., “Repairs” vs “Maintenance”)

With AI underwriting models in commercial real estate, this process becomes automated. For example, tools like Claude are now being used for Excel-based CRE underwriting automation, especially when standardizing financial data.

The system:

-

Maps similar categories into standard formats

-

Fills missing values based on patterns

-

Removes duplicates

-

Aligns all data into a consistent structure

For example, if one document lists “Utilities” and another lists “Electric + Water,” AI can group them correctly under one category. This creates a clean dataset that is ready for modeling.

Step 4: Financial Model Generation

After cleaning, the system builds the underwriting model. This is one of the biggest advantages of AI underwriting models in commercial real estate.

Instead of building models manually in Excel, AI generates:

-

Net Operating Income (NOI)

-

Cap rate calculations

-

Cash flow projections

-

IRR and return metrics

The model is structured and ready to review. It also follows consistent logic across deals. That means better comparability between properties.

Typical outputs include:

-

Year-by-year cash flow

-

Expense ratios

-

Vacancy assumptions

-

Revenue growth projections

This step reduces hours of modeling work into minutes.

Step 5: Validation and Error Checking

Even clean models need validation. AI underwriting models in commercial real estate include built-in checks to improve accuracy.

The system can:

-

Flag missing or unusual values

-

Identify inconsistencies between documents

-

Highlight outliers in income or expenses

-

Cross-check extracted data with source files

For example, if a rent roll shows higher income than the T12, the system flags it for review. This helps teams catch issues early. Instead of manually reviewing every line, analysts focus only on flagged items.

Step 6: Output: Clean, Investment-Ready Model

At the end of the process, the system produces a structured underwriting model.

This output is:

-

Clean and standardized

-

Easy to review

-

Ready for investment decisions

It can be exported into:

-

Excel

-

Internal dashboards

-

Investment memos

This is where AI underwriting models in commercial real estate deliver the most value. Instead of spending time preparing data, teams spend time evaluating deals.

Comparison: Output Quality Before vs After AI

| Aspect | Manual Output | AI Underwriting Models in Commercial Real Estate |

|---|---|---|

| Data Consistency | Varies across analysts | Standardized across all deals |

| Error Rate | Higher due to manual entry | Lower with automated checks |

| Model Structure | Depends on individual templates | Uniform and repeatable |

| Review Time | Long and detailed | Focused on flagged issues |

| Decision Readiness | Delayed | Immediate |

Real Tools Powering AI-Based Underwriting Today

AI underwriting models in commercial real estate are supported by a growing set of tools. However, most professionals only use a small part of what these tools can do.

AI Underwriting Platforms in the Market

Several platforms are built specifically for underwriting automation.

Popular categories include:

-

Data extraction tools

-

Financial modeling platforms

-

End-to-end underwriting systems

These tools focus on reducing manual work and improving speed. However, most tools still require proper setup and training to be effective.

Categories of CRE AI Tools

AI underwriting models in commercial real estate are not powered by a single tool. They rely on a combination of systems.

1. Document Intelligence Tools

-

Extract data from PDFs and scanned files

-

Handle leases, rent rolls, and reports

2. Financial Modeling Tools

-

Generate underwriting models

-

Calculate returns and projections

3. Market Data Platforms

-

Provide comps and benchmarks

-

Support assumption building

4. Deal Management Tools

-

Track pipelines

-

Organize deal flow

When combined, these tools create a full underwriting workflow.

Why Most Tools Still Fall Short

Even with strong technology, many firms struggle to see results.

The problem is not the tools. It is how they are used.

Common issues include:

-

Teams do not understand workflows

-

Tools are used in isolation

-

No standard process across deals

-

Lack of training

As a result, firms invest in software but still rely on manual work. This is why AI underwriting models in commercial real estate require more than just tools. They require structured implementation.

Our Approach: Training CRE Professionals to Use AI Effectively

At AI for CRE Collective, the focus is not just on tools. It is on building repeatable systems. AI underwriting models in commercial real estate only work when teams understand how to apply them.

Tools Alone Don’t Create Efficiency — Systems Do

Many firms make the same mistake. They buy tools and expect results. But without a workflow, tools create confusion instead of efficiency.

A proper system includes:

-

Defined steps

-

Clear inputs and outputs

-

Standard templates

-

Review processes

This is what turns AI into a real advantage.

How We Teach AI for CRE

Our training focuses on real-world applications.

We teach:

-

How to process raw financials using AI

-

How to clean and structure data

-

How to generate underwriting models

-

How to review and validate outputs

The goal is simple. Make AI underwriting models in commercial real estate usable in daily work.

Who Benefits from AI Training

AI is not limited to analysts.

Different roles benefit in different ways:

-

Investors improve deal evaluation speed

-

Brokers analyze deals before presenting them

-

Developers test project feasibility faster

-

Asset managers track performance more efficiently

-

Architects understand financial feasibility early

This creates alignment across the entire deal lifecycle.

Feature Comparison: Tools vs Trained Workflow

| Factor | Using Tools Only | Using AI with Structured Training |

|---|---|---|

| Efficiency | Limited improvement | Significant time savings |

| Consistency | Varies by user | Standardized across the team |

| Adoption | Low | High |

| Output Quality | Inconsistent | Reliable and repeatable |

| ROI on Tools | Unclear | Measurable |

AI underwriting models in commercial real estate are not just about automation. They are about changing how work gets done.

Key Benefits of AI Underwriting Models in Commercial Real Estate

AI underwriting models in commercial real estate are not just about saving time. They improve how decisions are made across the entire deal lifecycle.

When used correctly, these systems change both speed and quality of analysis. Here’s a practical example of how AI is speeding up feasibility and deal analysis in real scenarios:

Speed: From Hours to Minutes

Speed is the most visible benefit. In traditional workflows, underwriting a single deal can take several hours. In some cases, it takes days if the data is messy.

With AI underwriting models in commercial real estate:

-

Data extraction happens in minutes

-

Cleaning is automated

-

Models are generated instantly

This allows teams to review more deals in less time.

In practice:

-

Analysts can evaluate multiple deals in a day

-

Firms respond faster to opportunities

-

Deal pipelines move more efficiently

Speed also creates a competitive edge. In CRE, timing often decides who wins a deal.

Accuracy and Reduced Human Error

Manual underwriting always carries risk.

Even experienced analysts can make mistakes when:

-

Entering data

-

Copying formulas

-

Adjusting assumptions

AI underwriting models in commercial real estate reduce these risks.

The system:

-

Pulls data directly from source documents

-

Applies consistent logic

-

Flags inconsistencies automatically

This leads to more reliable outputs.

Key improvements include:

-

Fewer calculation errors

-

Better alignment across documents

-

Clear audit trails

Accuracy improves confidence in decisions.

Better Decision-Making with Structured Data

Clean data leads to better insights. When data is structured, it becomes easier to analyze trends and compare deals.

AI underwriting models in commercial real estate provide:

-

Standardized financial models

-

Clear breakdowns of income and expenses

-

Scenario-based projections

This allows decision-makers to focus on strategy instead of data preparation.

Examples:

-

Comparing multiple properties side by side

-

Testing different rent growth assumptions

-

Evaluating risk under different scenarios

The result is more informed decision-making.

Cost Reduction Across Teams

Efficiency leads to cost savings. In traditional setups, firms rely heavily on junior analysts for data work. This increases operational costs.

With AI underwriting models in commercial real estate:

-

Fewer manual hours are needed

-

Smaller teams can handle more deals

-

Senior professionals spend time on strategy

This reduces overall workload without reducing output.

Scalability Across Deal Pipelines

As deal volume grows, manual systems struggle. AI makes scaling easier.

Teams can:

-

Analyze more deals without increasing headcount

-

Maintain consistency across all models

-

Standardize workflows across offices

This is especially useful for firms handling high deal flow.

Benefit Comparison: Before vs After AI Adoption

| Area | Before AI | After AI Underwriting Models in Commercial Real Estate |

|---|---|---|

| Speed | Slow, manual | Fast and automated |

| Accuracy | Dependent on the analyst | System-driven with validation |

| Cost | High labor dependency | Reduced operational cost |

| Deal Volume | Limited | Scalable |

| Decision Quality | Inconsistent | Data-driven and structured |

Real-World Use Cases of AI in CRE Underwriting

AI underwriting models in commercial real estate are already being used in different parts of the industry. These are not future concepts. They are active workflows.

Deal Screening at Scale

Firms receive a large number of deals every week. Manually reviewing each one is not practical.

AI helps by:

-

Quickly extracting key data

-

Generating initial models

-

Ranking deals based on criteria

This allows teams to focus only on high-potential opportunities.

Investment Committee Preparation

Preparing investment memos takes time. AI underwriting models in commercial real estate simplify this process.

They can:

-

Summarize financial performance

-

Highlight key risks

-

Generate structured reports

This reduces preparation time and improves clarity during discussions.

Portfolio Analysis

Managing multiple assets requires consistent data. AI makes it easier to analyze entire portfolios.

Teams can:

-

Compare asset performance

-

Identify underperforming properties

-

Track trends across regions

This helps in making better asset management decisions.

Risk Assessment and Early Issue Detection

Risk identification is critical in underwriting.

AI systems help detect issues early.

They can flag:

-

Income inconsistencies

-

Unusual expense patterns

-

Missing lease data

-

Outliers in projections

This allows teams to address risks before making decisions.

Use Case Breakdown

| Use Case | Traditional Approach | AI-Based Approach |

|---|---|---|

| Deal Screening | Manual review of each deal | Automated filtering and ranking |

| Investment Memos | Built manually | Generated using structured data |

| Portfolio Analysis | Spreadsheet-based | Real-time dashboards |

| Risk Detection | Manual checks | Automated alerts and flags |

Challenges and Limitations of AI in CRE

While AI underwriting models in commercial real estate offer clear benefits, they are not perfect. Understanding limitations is important for proper use.

Data Quality Issues

AI depends on input data. If the data is incomplete or incorrect, the output will reflect that.

Common issues include:

-

Missing lease details

-

Incorrect financial entries

-

Poorly formatted documents

AI can reduce errors, but it cannot fix fundamentally bad data.

Over-Reliance on Automation

Automation improves efficiency, but it should not replace judgment. AI underwriting models in commercial real estate still require human review.

Professionals must:

-

Validate assumptions

-

Interpret results

-

Make final decisions

AI supports analysis. It does not replace expertise.

Integration with Existing Systems

Many firms already use tools like Excel and legacy systems. Integrating AI into existing workflows can be challenging.

Issues may include:

-

Data transfer between systems

-

Compatibility with current tools

-

Resistance to change within teams

Proper implementation is key to overcoming this.

Learning Curve for Teams

Adopting AI requires learning.

Teams need to understand:

-

How the system works

-

How to review outputs

-

How to adjust workflows

Without training, adoption remains low. This is one of the biggest barriers to using AI underwriting models in commercial real estate effectively.

Limitation Overview

| Challenge | Impact | Solution Approach |

|---|---|---|

| Data Quality | Inaccurate outputs | Improve data collection processes |

| Over-Reliance | Poor decision-making | Maintain human review |

| Integration Issues | Workflow disruption | Gradual implementation |

| Learning Curve | Low adoption | Training and structured workflows |

AI underwriting models in commercial real estate are powerful, but they work best when combined with the right processes and training.

The Future of AI Underwriting Models in Commercial Real Estate

AI underwriting models in commercial real estate are still evolving. What we see today is only the early stage. The next phase will focus less on single tools and more on connected systems.

The shift is already happening. Workflows are becoming more automated, and decisions are becoming more data-driven.

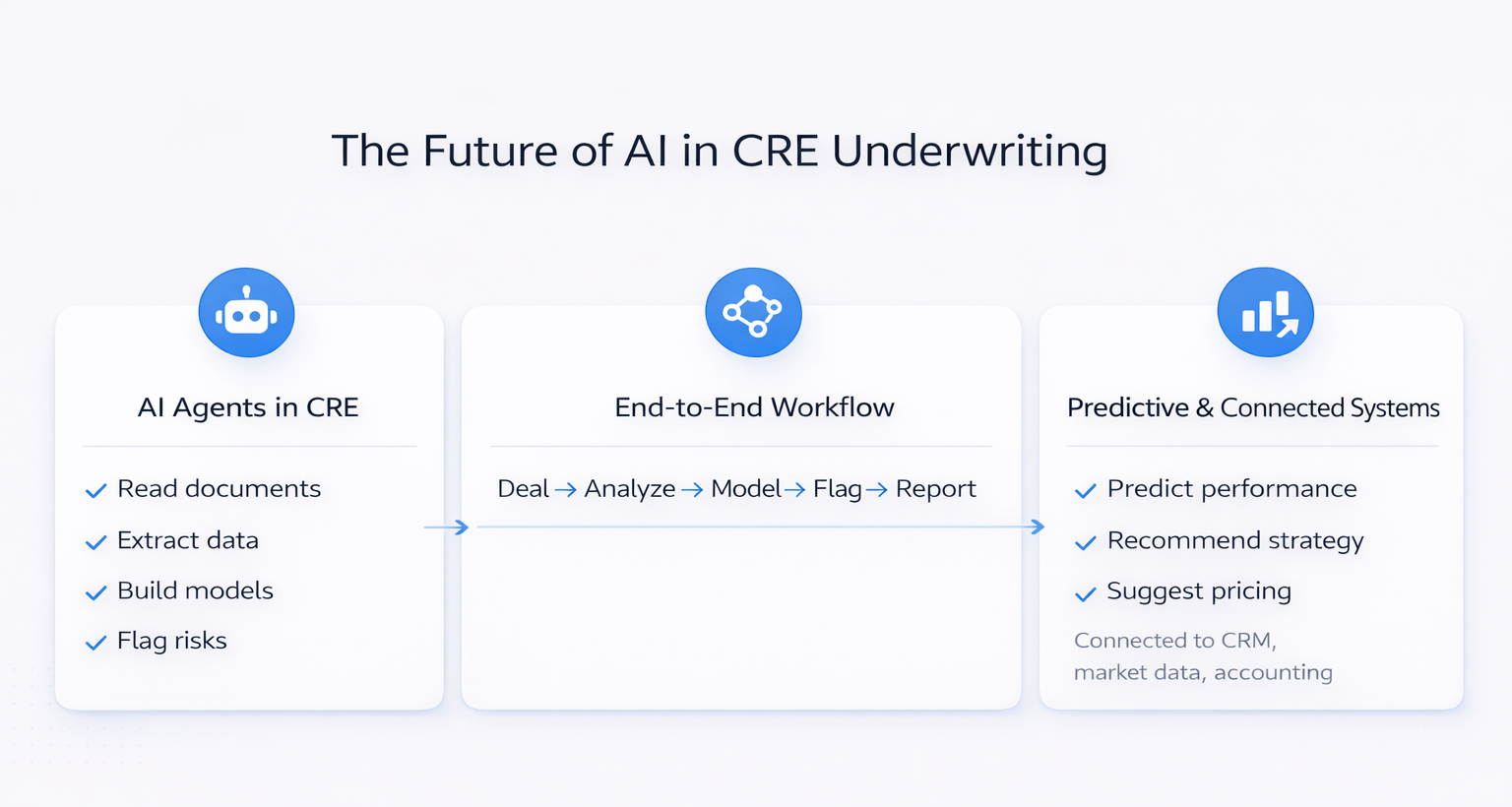

Rise of AI Agents in CRE

One major change is the use of AI agents. Instead of running one task at a time, AI agents handle multiple tasks together.

For example, a single system can:

-

Read documents

-

Extract financial data

-

Build a model

-

Flag risks

-

Generate a summary

All of this happens in one flow. AI underwriting models in commercial real estate are moving toward these multi-step systems. This reduces the need for switching between tools.

End-to-End Automation of Deal Workflows

Today, underwriting is just one part of the process.

In the future, AI will connect:

-

Deal sourcing

-

Underwriting

-

Investment decisions

-

Asset management

This creates a full pipeline. Instead of isolated steps, everything will be connected.

Example workflow:

-

A deal is uploaded

-

AI extracts and analyzes data

-

A model is created

-

Risks are flagged

-

A report is generated

-

The deal is pushed to decision-makers

This reduces delays and improves coordination across teams.

Predictive and Prescriptive Analytics

Current systems analyze past and present data. Future AI underwriting models in commercial real estate will go further.

They will:

-

Predict future performance

-

Suggest optimal strategies

-

Recommend pricing or exit timing

This adds another layer of value. Instead of just showing numbers, systems will guide decisions.

Integration with the Full CRE Tech Stack

Another key shift is integration.

AI will connect with:

-

CRM systems

-

Market data platforms

-

Accounting tools

-

Asset management software

This creates a unified environment. Data flows smoothly between systems, reducing duplication and errors.

Future vs Current State Comparison

| Area | Current State | Future with AI Underwriting Models in Commercial Real Estate |

|---|---|---|

| Workflow Structure | Fragmented tools | Fully connected systems |

| Automation Level | Partial | End-to-end automation |

| Decision Support | Data analysis | Predictive and prescriptive insights |

| Data Flow | Manual transfers | Seamless integration |

| Role of Analysts | Data preparation + analysis | Strategy and decision-making |

How to Get Started with AI Underwriting Models in Commercial Real Estate

Many professionals understand the value of AI, but they are unsure where to begin. The key is to start simple and build gradually.

Step 1: Identify Bottlenecks in Your Workflow

Start by reviewing your current process. Look for areas where time is wasted.

Common bottlenecks include:

-

Data extraction from PDFs

-

Cleaning inconsistent financials

-

Building models manually

These are the best starting points for AI adoption.

Step 2: Start with One Use Case

Do not try to change everything at once. Focus on one task.

For example:

-

Automating rent roll extraction

-

Standardizing T12 analysis

This helps teams see results quickly. Once one process works well, you can expand further.

Step 3: Choose the Right Tools (Not Too Many)

It is easy to get overwhelmed with tools.

Instead, focus on:

-

Tools that solve your main problem

-

Systems that integrate with your workflow

Avoid adding multiple tools without a clear plan.

Step 4: Learn the Workflow, Not Just the Tool

This is where many teams struggle.

Knowing how a tool works is not enough.

You need to understand:

-

How data flows through the system

-

How outputs are generated

-

How to validate results

AI underwriting models in commercial real estate are most effective when used within a structured workflow.

Step 5: Scale Across Your Team

Once a workflow is working, expand it.

This includes:

-

Standardizing processes

-

Training team members

-

Applying the system across deals

This ensures consistency and long-term results.

Getting Started Roadmap

| Step | Action | Outcome |

|---|---|---|

| Identify Bottlenecks | Review current workflow | Clear starting point |

| Start Small | Focus on one use case | Quick results |

| Select Tools | Choose relevant solutions | Avoid complexity |

| Learn Workflow | Understand the full process | Better implementation |

| Scale | Expand across the team | Consistent and scalable system |

Why AI Training is the Competitive Advantage in CRE Today

Technology alone does not create an advantage. How it is used makes the difference. AI underwriting models in commercial real estate are available to many firms. But not all firms use them effectively.

The Gap Between Tools and Implementation

Most professionals face the same issue.

They have access to tools but lack a clear system.

This leads to:

-

Low adoption

-

Inconsistent results

-

Limited efficiency gains

Bridging this gap requires training.

Early Adopters Will Win More Deals

Speed matters in CRE.

Firms that adopt AI underwriting models in commercial real estate early can:

-

Analyze deals faster

-

Respond quicker

-

Make decisions with confidence

This increases their chances of securing better opportunities.

AI Literacy is Becoming a Core CRE Skill

In the past, Excel was a key skill.

Today, AI is becoming just as important.

Professionals who understand AI workflows can:

-

Work more efficiently

-

Handle more deals

-

Provide better insights

This creates long-term career value.

Training vs No Training Comparison

| Factor | Without Training | With AI Training |

|---|---|---|

| Tool Usage | Limited | Effective |

| Workflow Understanding | Low | High |

| Efficiency Gains | Minimal | Significant |

| Team Adoption | Slow | Faster |

| ROI on AI | Unclear | Measurable |

Final Thoughts: From Spreadsheets to Smart Systems

AI underwriting models in commercial real estate are changing how deals are analyzed. The shift is clear. Work that once took hours now takes minutes. Data that was messy is now structured. Decisions that were delayed are now faster and more informed.

However, the real value comes from how these systems are used. Firms that combine:

-

The right tools

-

Clear workflows

-

Proper training

will see the biggest results.

At AI for CRE Collective, the focus is on helping professionals apply AI in real underwriting scenarios. The goal is not just to use technology, but to improve how work gets done. AI underwriting models in commercial real estate are not just a trend. They are becoming a standard part of the industry.

The sooner teams adapt, the stronger their position will be in an increasingly competitive market.