How to Write AI-Ready Acquisition Criteria for Multifamily Deals

Most AI underwriting attempts fail before they even start. The prompts are vague, assumptions are scattered, and key inputs often live in someone’s head. As a result, even an AI underwriting criteria document is often missing or incomplete, causing tools to generate generic outputs that do not reflect how deals are actually evaluated.

This is where an AI underwriting criteria document becomes essential. Instead of relying on incomplete inputs, you create a single source of truth that captures every assumption, threshold, and methodology used in your underwriting process.

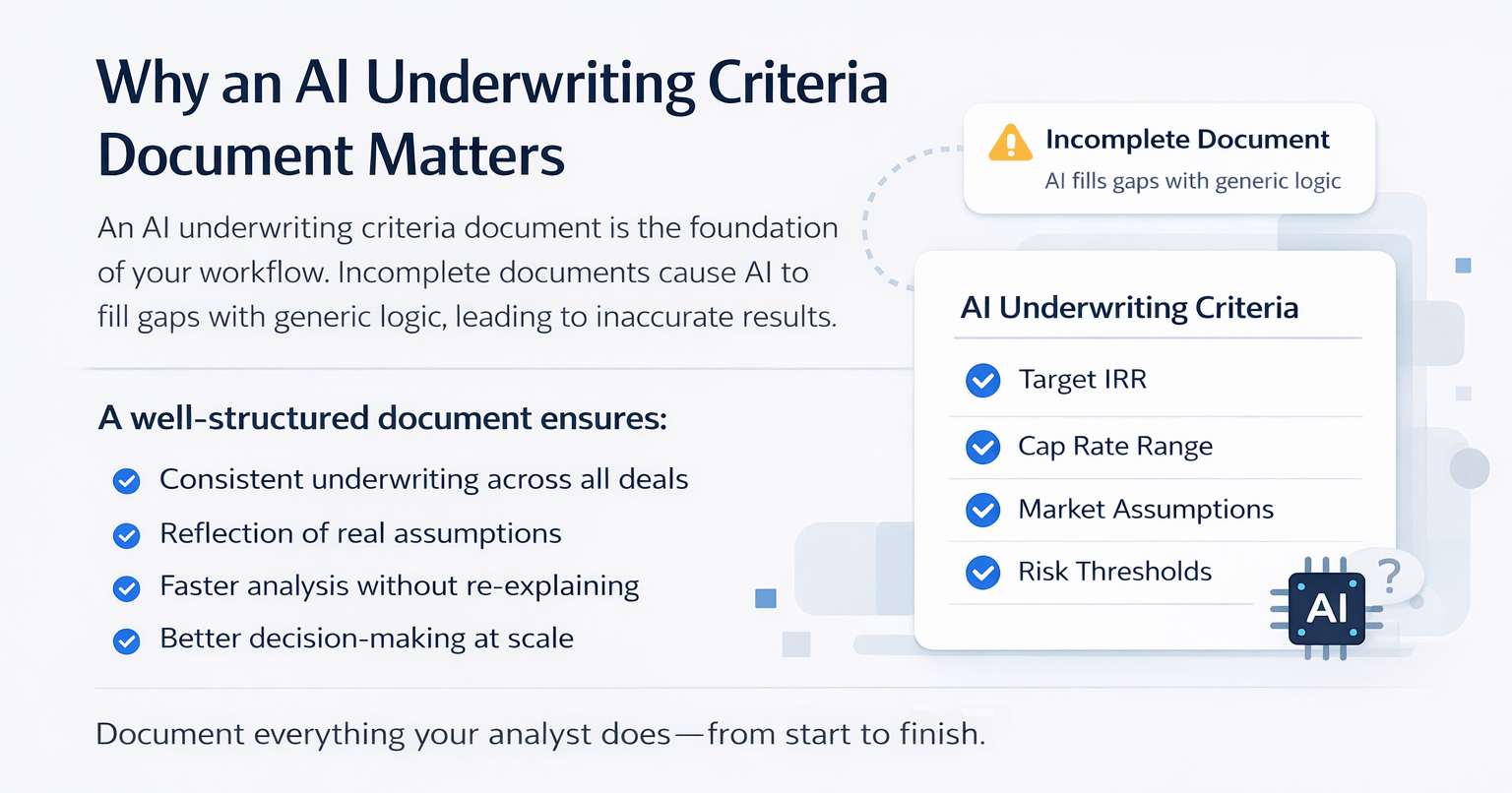

Why an AI Underwriting Criteria Document Matters

When building an AI underwriting workflow, your criteria document becomes the foundation. Every assumption and decision flows from it. Therefore, if the document is incomplete, the AI fills gaps with generic logic, which leads to unusable results.

In contrast, a well-structured document ensures:

- Consistent underwriting across all deals

- Accurate reflection of your real assumptions

- Faster analysis without re-explaining the methodology

- Better decision-making at scale

Ultimately, the goal is simple: document everything your analyst does from start to finish.

Markdown vs Word: Why Format Matters

Before diving into the content, formatting plays a critical role. While Word documents can work, markdown files are far more efficient for AI tools.

Key Differences

| Format | Benefits | Limitations |

|---|---|---|

| Markdown (.md) | Lightweight, AI-friendly, low token usage | Requires basic formatting knowledge |

| Word Docs | Familiar interface | Higher token cost, less efficient |

Because AI tools process markdown more efficiently, using it reduces token usage and improves performance over time.

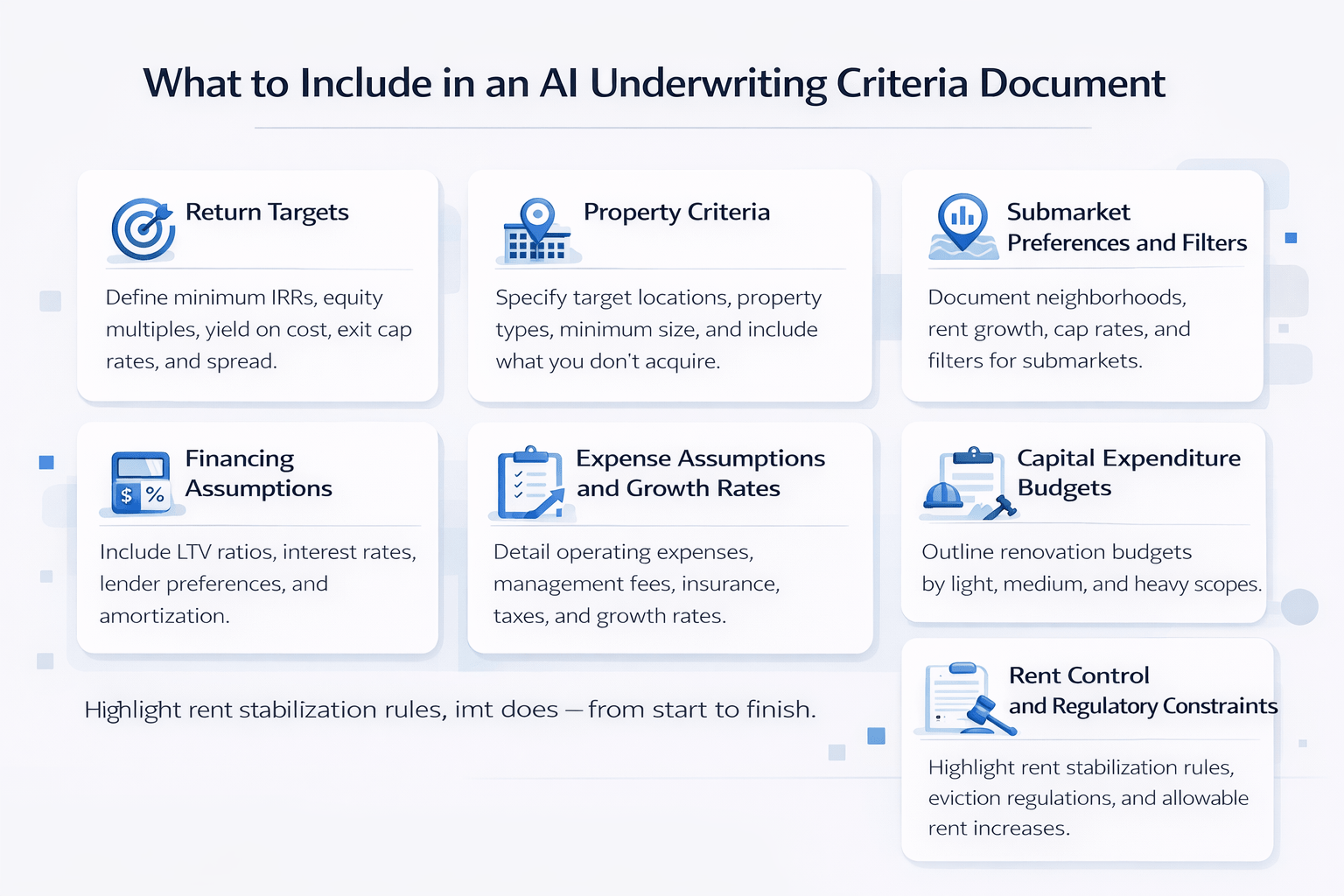

What to Include in an AI Underwriting Criteria Document

To build a strong AI underwriting criteria document, you need to capture every component of your deal analysis process. Below is a structured breakdown.

Return Targets

Start with the numbers that define whether a deal works. These act as your initial screening thresholds.

- Minimum levered IRR: 15%

- Minimum equity multiple: 1.5x

- Yield on cost: 7%

- Exit cap rate range: 5.5%–7%

- Minimum spread: 150 basis points

These metrics allow AI to quickly determine whether a deal meets your investment criteria.

Property Criteria

Next, clearly define what types of assets you target.

- Location: LA County

- Property type: Apartments

- Minimum size: 5+ units

- Year built: 1920 or newer

- Class: B and C

Equally important, define what you do NOT acquire. This prevents unnecessary analysis and saves time.

Submarket Preferences and Filters

Local expertise must be documented. Otherwise, AI cannot replicate it.

Include:

- Target neighborhoods

- Rent growth assumptions by area

- Cap rate ranges by submarket

This section transforms your experience into structured data.

Financing Assumptions

Every underwriting model depends on financing inputs.

- Loan-to-value ratios

- Interest rate assumptions

- Lender preferences

- Amortization terms

Without these inputs, AI defaults to generic assumptions, which makes outputs unreliable.

Expense Assumptions and Growth Rates

Expense modeling is where most AI tools fail. Therefore, this section must be highly detailed.

- Operating expenses per unit

- Property management fees

- Insurance costs

- Property taxes

- Utility expenses

- Annual growth rates

Accurate expense assumptions are critical for realistic underwriting results.

Capital Expenditure Budgets

Capex planning should be broken down by renovation level.

- Light renovation: $10K–$20K per unit

- Medium renovation: Defined scope and budget

- Heavy renovation: Full repositioning scope

Include both unit interiors and exterior/common area improvements. The more detail you provide, the better the AI projections.

Rent Control and Regulatory Constraints

In regulated markets, this section is essential.

- Rent stabilization rules

- Allowable rent increases

- Eviction regulations

- Relocation requirements

Without this information, AI may overestimate revenue potential.

Tenant Buyout Strategy

This is one of the most overlooked but valuable sections.

- Define when buyouts are used

- Set typical buyout ranges

- Map rent delta to buyout cost

For example:

| Rent Delta (Monthly) | Estimated Buyout |

|---|---|

| $400 | ~$18,000 |

| $850 | ~$36,000 |

This level of detail allows AI to perform unit-level analysis instead of broad estimates.

Putting the Criteria Document Into Production

Once completed, your AI underwriting criteria document becomes the backbone of your workflow. Every deal is evaluated using the same assumptions and methodology.

As a result:

- Underwriting becomes consistent

- Time spent re-explaining logic is eliminated

- Deal evaluation speed increases significantly

Although the initial setup may take a few hours, the long-term efficiency gains are substantial.

FAQs Regarding AI Underwriting Criteria Document

What is an AI underwriting criteria document?

It is a structured document that defines all assumptions used in deal analysis.

- Includes return targets

- Covers expenses and financing

- Guides AI decision-making

Conclusion: It ensures consistent and accurate underwriting.

https://www.investopedia.com

Why do AI underwriting tools fail?

They fail due to incomplete or vague inputs.

- Missing assumptions

- Scattered data sources

- Lack of structure

Conclusion: A strong criteria document solves this issue.

https://www.mckinsey.com

Is markdown better than Word for AI workflows?

Yes, markdown is more efficient for AI processing.

- Lower token usage

- Cleaner structure

- Faster performance

Conclusion: Markdown improves efficiency and reduces cost.

https://www.markdownguide.org

What should be included in the document?

It should cover every aspect of underwriting.

- Returns

- Expenses

- Financing

- Market assumptions

Conclusion: Include everything your analyst uses.

https://www.nar.realtor

How long does it take to create one?

It typically takes a few hours initially.

- One-time effort

- Long-term efficiency gains

- Scalable output

Conclusion: Time investment pays off quickly.

https://www.forbes.com

Can this work for all property types?

Yes, with customization for each asset class.

- Multifamily

- Office

- Retail

Conclusion: Adapt the structure to your strategy.

Does it replace financial models?

No, it enhances them.

- Provides inputs

- Improves consistency

- Reduces errors

Conclusion: It complements underwriting models.

https://www.asce.org

How does it improve deal flow?

It speeds up and standardizes analysis.

- Faster screening

- Consistent outputs

- Better decision-making

Conclusion: It improves both speed and accuracy.

Build Consistency Into Your Underwriting Workflow

Join AI for CRE, where 663+ CRE professionals are already using structured criteria documents and AI workflows to standardize underwriting, eliminate inconsistent outputs, and scale their deal pipelines.

Access real templates, proven underwriting systems, and step-by-step frameworks that help you turn scattered assumptions into a repeatable, reliable process. Instead of relying on generic AI outputs, you can build a system that reflects exactly how your team evaluates deals—every time.