Bridge to Perm vs Permanent Debt on Vacant Multifamily

If you’re deciding between financing options for a vacant deal, the bridge vs permanent debt strategy can determine whether your investment succeeds or struggles. Choosing between these two approaches is not just about rates—it directly impacts cash flow, risk, and execution.

I recently tested this on a 7-unit multifamily deal in Long Beach, California, using AI. After analyzing five lender term sheets, the results made the answer clear: financing structure matters just as much as the interest rate.

The Deal Setup

Here’s the scenario analyzed:

- 7-unit multifamily property

- Located in Long Beach, California

- Built in 1962

- Purchase price: $3.9M

- Price per unit: ~$557K

- 100% vacant

We received five lender term sheets ranging from:

- 5.95% fixed permanent loan

- 85% LTC bridge loan (SOFR + 350)

This created a strong comparison case.

The Problem with Permanent Debt on Vacant Properties

At first glance, permanent debt seems attractive due to lower rates. However, it introduces major risks for vacant assets.

Key Issues

- Requires immediate principal and interest payments

- No rental income to support debt service

- Higher upfront cash requirements

For example:

- Cash to close: ~$1.7M

- Full amortizing payments from day one

Therefore, investors must fund debt service out of pocket during lease-up.

Bridge vs Permanent Debt Strategy Comparison

| Factor | Permanent Debt | Bridge Loan |

|---|---|---|

| Interest Rate | Lower (fixed) | Higher (floating) |

| Payments | Principal + Interest | Interest-only |

| Cash Flow Impact | Negative during vacancy | Preserved during lease-up |

| Flexibility | Low | High |

| Close Speed | Slower | Faster |

| Risk Type | Cash flow strain | Refinance risk |

As a result, each option serves a different strategy.

The Bridge-to-Perm Alternative

A bridge loan provided a more practical solution for this deal.

Key Features

- 75% LTV financing

- Interest-only payments

- 6-month interest reserve

- $200K renovation holdback

- Faster closing timeline

Trade-Offs

- Higher rate (~7.85%)

- Full recourse

- Short-term structure (2+1 years)

However, it aligned better with the lease-up business plan.

The Two-Step Strategy

The AI analysis recommended a bridge-to-perm strategy.

Phase 1: Bridge Loan

- Preserve cash during vacancy

- Fund renovations

- Stabilize occupancy

Phase 2: Refinance

- Transition to permanent debt

- Lock a lower rate

- Reduce long-term risk

This approach balances flexibility with long-term stability.

Cost Comparison Breakdown

| Cost Component | Bridge Strategy | Permanent Loan |

|---|---|---|

| Cash to Close | ~$1.3M | ~$1.7M |

| Interest Cost | Higher | Lower |

| Total Cost Difference | +~$75K | Lower upfront |

| Cash Flow Impact | Positive (protected) | Negative |

Although the bridge costs more, it reduces early-stage financial pressure.

Why the Lowest Rate Was Not the Best Option

The lowest rate lender offered:

- 5.95% fixed

- Long-term stability

However, it required:

- High cash to close

- Immediate amortization

- Strong liquidity

Meanwhile, the bridge lender:

- Supported lease-up

- Preserved cash

- Funded renovations

Therefore, the higher-rate option was strategically better.

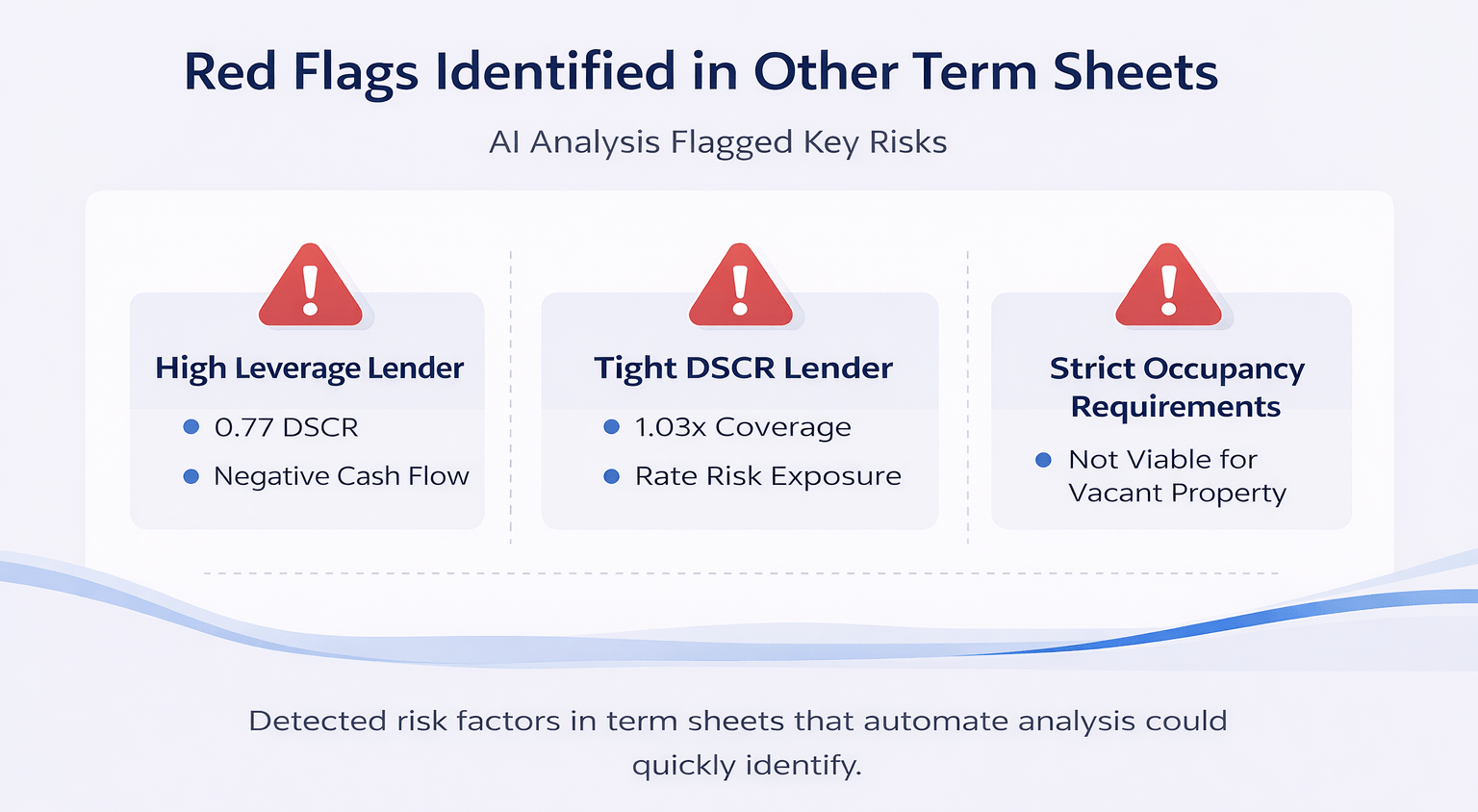

Red Flags Identified in Other Term Sheets

The AI analysis flagged several risks:

- High leverage lender

- 0.77 DSCR

- Negative cash flow

- Tight DSCR lender

- 1.03x coverage

- Rate risk exposure

- Strict occupancy requirements

- Not viable for vacant property

These insights are difficult to identify quickly without automation.

When Permanent Debt Still Makes Sense

Permanent financing can work if:

- The property has 70–80% occupancy

- Lease-up timeline is short

- Strong cash reserves are available

In these cases:

- Lower rates improve returns

- Long-term stability is beneficial

Key Takeaways

- Financing strategy matters more than rate

- Bridge loans support execution during vacancy

- Permanent loans require a stable income

- AI analysis improves decision-making speed

Overall, aligning financing with your business plan is critical.

FAQs Regarding Bridge vs Permanent Debt Strategy

What is a bridge vs permanent debt strategy?

It is a financing decision between short-term flexible loans and long-term stable loans.

- Bridge loans support transitions

- Permanent loans provide stability

- Choice depends on deal conditions

It determines how effectively you execute your investment plan.

Why is permanent debt risky for vacant properties?

Because it requires immediate payments.

- No income during lease-up

- High cash burn

- Increased financial pressure

It can strain liquidity early in the investment.

What are the advantages of bridge loans?

They provide flexibility during transitions.

- Interest-only payments

- Renovation funding

- Faster closing

They help stabilize properties before refinancing.

What is a bridge-to-perm strategy?

It is a two-step financing approach.

- Use a bridge loan first

- Stabilize property

- Refinance into permanent debt

It aligns financing with the business plan.

When should you use permanent debt?

When the property is stabilized.

- Strong occupancy

- Predictable cash flow

- Lower risk

It works best for long-term holding strategies.

What is the biggest risk of bridge loans?

Refinancing risk.

- Short-term structure

- Market dependency

- Rate fluctuations

Proper timing is essential for success.

How does AI help in financing decisions?

AI analyzes multiple scenarios quickly.

- Compares term sheets

- Identifies risks

- Provides recommendations

It improves speed and accuracy.

What is the biggest takeaway from this strategy?

The structure matters more than the rate.

- Align financing with the business plan

- Focus on execution

- Manage risk effectively

It leads to better investment outcomes.

Build Smarter Financing Strategies

Join the AI for CRE Collective, where 600+ CRE professionals are using AI workflows like this to evaluate financing strategies, compare lender term sheets, and make smarter investment decisions backed by real data.

Get access to real prompts, deal breakdowns, and step-by-step workflows—so you can choose the right financing structure with confidence on every deal.